Running a business in Huntington means protecting your assets from multiple risks at once. A Business Owners Policy bundles the coverage you actually need-liability, property, and business interruption-into one affordable package.

At JW Hirschfeld Agency, Inc., we help local business owners find BOP coverage in Huntington, NY that fits their real situation. The right policy saves you money while keeping your operation secure.

What a Business Owners Policy Actually Covers

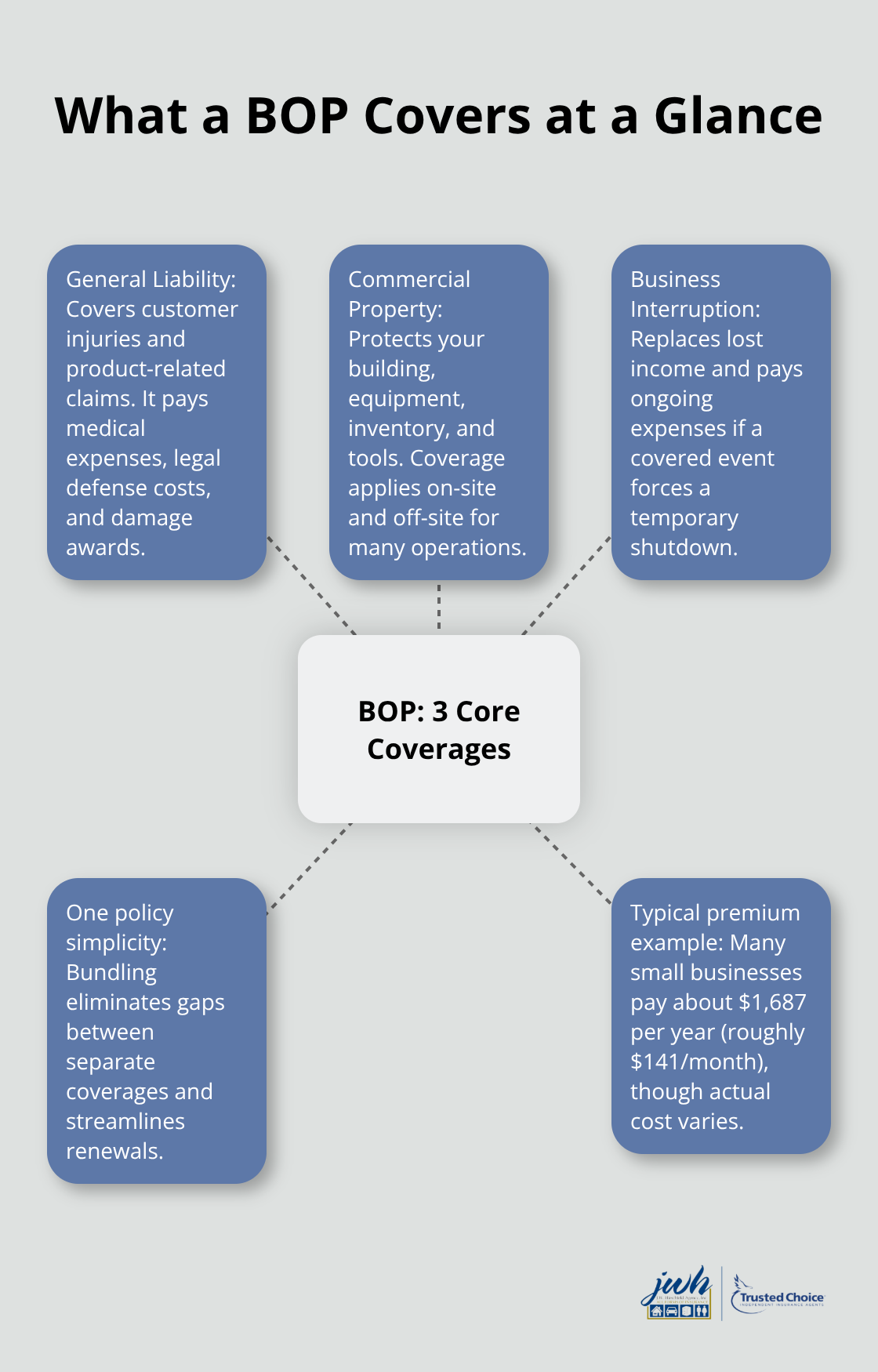

A Business Owners Policy combines three essential coverages into one package: General Liability, Commercial Property, and Business Interruption. General Liability protects you when a customer gets injured on your premises or claims your product caused them harm-it covers medical expenses, legal defense costs, and damage awards. Commercial Property covers your building structure, equipment, inventory, and tools, whether they’re at your location or off-site. Business Interruption replaces lost income and pays your ongoing expenses like rent or lease payments, employee wages, taxes, and loan payments if a covered disaster forces you to close temporarily. The Hartford reports that their BOP customers pay an average of $1,687 annually (roughly $141 per month), though your actual cost depends on your business type, location, and risk profile. This single policy approach eliminates gaps between separate coverages and simplifies your renewal process.

Why bundling saves real money for Huntington businesses

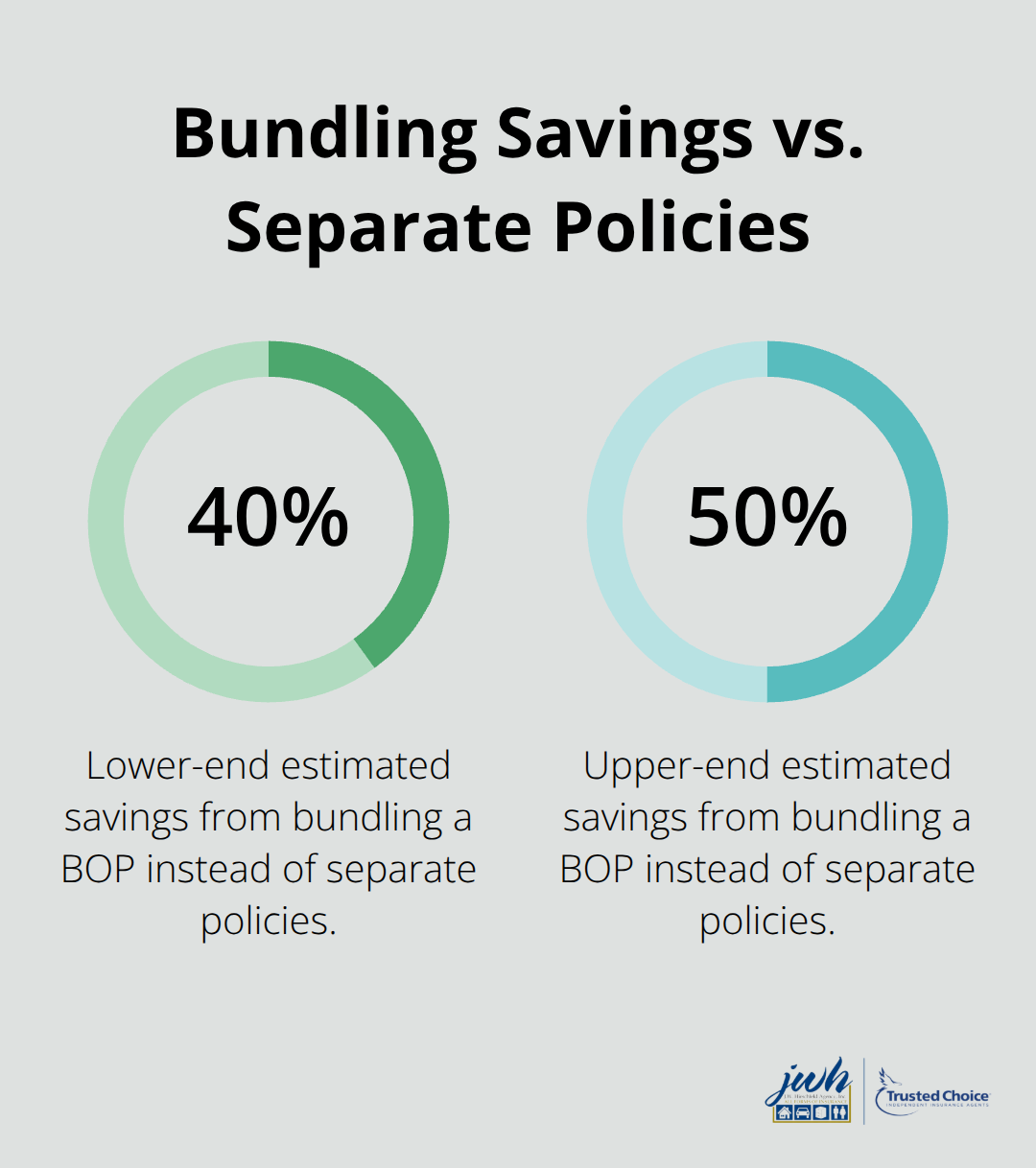

Separate coverage for these three components typically costs $8,000 to $12,000 per year, while a bundled BOP runs $3,000 to $7,000 annually. That’s a 40 to 50 percent reduction that goes straight to your bottom line.

Small to mid-size businesses in Huntington with fewer than 100 employees and under $5 million in annual revenue qualify for most BOP programs, including retailers, restaurants, contractors, professional offices, and service companies. An independent agent can adjust your coverage limits and deductibles to match your actual exposure, preventing you from overpaying for protection you don’t need or underinsuring critical assets. Many policies also include off-site tool coverage for contractors and data backup protection for professional offices-extras that would cost substantially more if purchased separately.

The practical advantage of one agent, one carrier

A single insurer through an independent agent eliminates coordination problems when you file a claim. You contact one person who manages your entire policy, coordinates with adjusters, and advocates for faster claim resolution. This matters most during disasters-when a Nor’easter hits Huntington and damages your roof while forcing temporary closure, one agent handles both property and business interruption claims, reducing stress and accelerating your recovery. The independent agent relationship also means someone local understands Long Island’s specific risks: coastal storms, flooding patterns, and industry-specific hazards. Rather than dealing with multiple carriers with conflicting timelines and requirements, you get streamlined communication and faster payouts.

What makes independent agents different

Independent agents like those at JW Hirschfeld Agency, Inc. represent multiple top carriers, which means they shop your coverage across different insurers to find the best rates and terms for your situation. This access to multiple options gives you competitive pricing that captive agents (who work for one company) simply cannot match. An independent agent also acts as your advocate during claims-they work for you, not the insurance company-and they know the local Huntington business landscape well enough to spot coverage gaps before problems occur. This local expertise combined with multi-carrier access creates a significant advantage when you’re trying to protect your business without overspending.

Which Huntington Businesses Need a BOP Most

Retail shops face constant customer liability exposure

Retail shops face constant exposure to customer injuries and product liability claims. A customer slips on a wet floor, a product defect causes harm, or someone claims your display caused property damage-these situations happen regularly in retail environments. General Liability within a BOP covers medical expenses and legal defense costs, while Commercial Property protects your inventory and fixtures from theft, fire, and weather damage.

Restaurants and hospitality venues operate under higher risk

Restaurants and hospitality venues operate under even higher risk because they combine food safety liability, customer injuries on premises, weather-related closures, and significant equipment investment. A single foodborne illness claim or kitchen fire can devastate operations; Business Interruption coverage covers loss of income while you rebuild. This combination of exposures makes a BOP essential for any food service operation in Huntington.

Service-based companies need off-site tool protection

Service-based companies like plumbing, HVAC, landscaping, and cleaning operations benefit because their work happens at client locations where liability exposure extends beyond their own premises. Off-site tool coverage within a BOP protects equipment and materials whether they’re at your shop or at a customer’s property, eliminating gaps that separate policies would create. This protection matters most for contractors who move between multiple job sites throughout Huntington.

Professional services require data and document protection

Professional services including accounting, law, real estate, and consulting firms need BOPs because they hold client documents, maintain sensitive data, and face property damage risks. Data backup protection included in many BOPs prevents the catastrophic loss of client files. Contractors-both general and specialty trades-face completed operations liability where claims arise months or years after project completion due to alleged workmanship issues.

Coverage tailoring prevents overpaying and underpaying

Bundled BOPs save small businesses compared to purchasing coverages separately, and eligibility extends to most Huntington businesses with fewer than 100 employees and under $5 million in annual revenue. Your specific business type, location, inventory value, and staffing levels determine which coverages matter most and what limits you actually need. An independent agent assesses your exact operation-not a generic business profile-and recommends coverage that matches your real exposure, preventing overpaying for unnecessary protection while keeping critical gaps closed. The next step involves understanding how to select the right BOP limits and deductibles for your specific Huntington operation.

Choosing the Right BOP Limits for Your Huntington Business

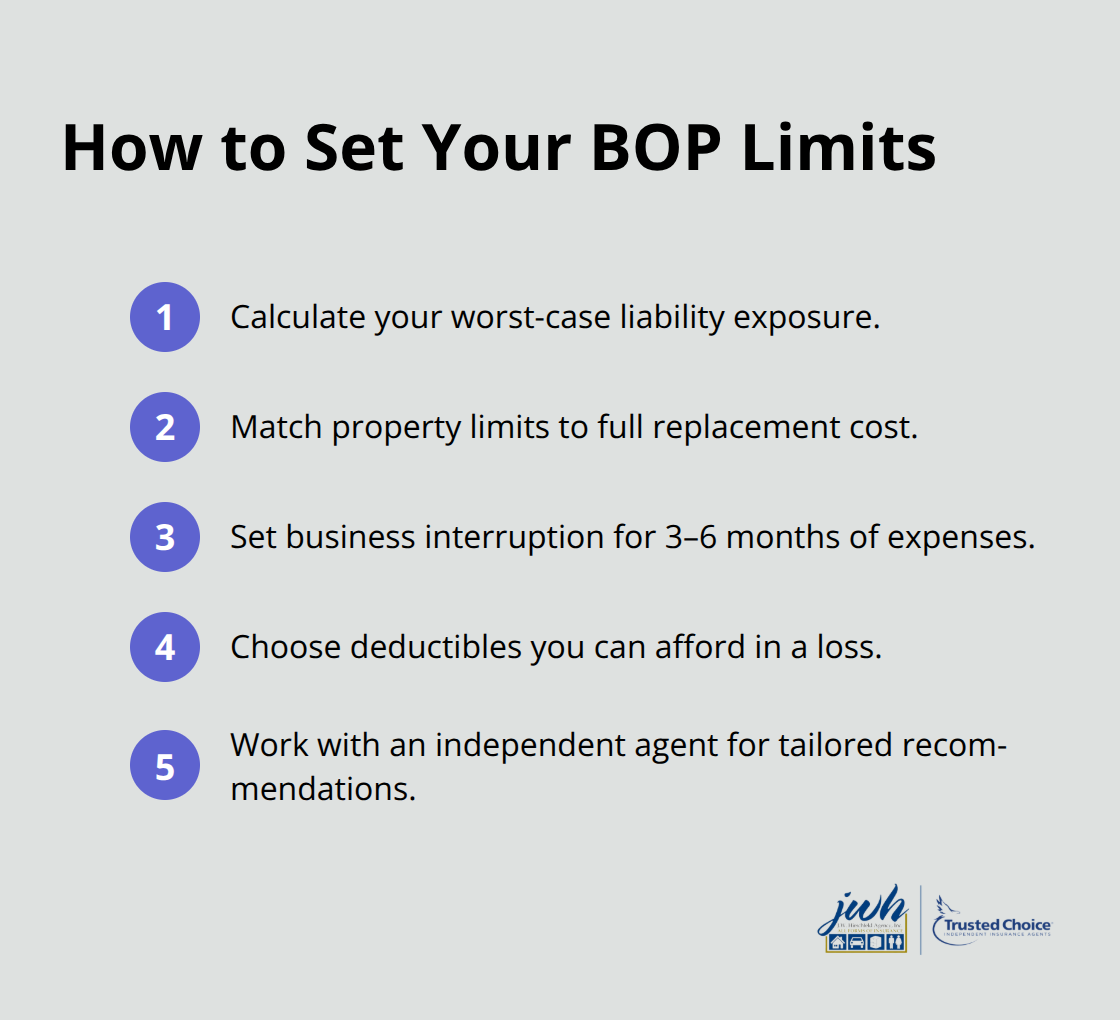

Selecting a BOP isn’t about picking the cheapest option-it’s about matching your coverage limits and deductibles to what actually happens in your operation. Most Huntington business owners make the mistake of either accepting whatever limits their quote suggests or copying what a competitor carries, neither of which reflects their real exposure.

Calculate your liability exposure realistically

Start by calculating your potential liability: if a customer sues for bodily injury, what’s your worst-case scenario? For a restaurant, that might be a serious food poisoning claim reaching $500,000. For a retail shop, a slip-and-fall could generate $250,000 in medical and legal costs. General Liability limits typically range from $300,000 to $2 million per occurrence, with most small businesses in Huntington choosing $1 million as a reasonable middle ground.

Match property limits to replacement costs

Your Commercial Property limit should equal the replacement cost of your building (if you own it), equipment, inventory, and fixtures-not the depreciated value. An HVAC contractor with $150,000 in tools and equipment needs that amount covered, plus replacement cost for any inventory. This prevents the painful discovery that your coverage falls short when you actually need to rebuild.

Set business interruption coverage for realistic recovery

Business Interruption coverage should replace at least three to six months of operating expenses: payroll, rent, utilities, loan payments, and taxes. If your monthly overhead runs $8,000, try for at least $24,000 to $48,000 in Business Interruption limits. This ensures you can maintain operations while recovering from a covered disaster.

Choose deductibles you can actually afford

Deductibles work inversely with premiums-a $1,000 deductible costs more than a $2,500 deductible-so select what you can actually afford to pay out-of-pocket during a loss. Many Huntington contractors choose $2,500 deductibles to keep premiums reasonable while maintaining manageable out-of-pocket risk.

Work with an independent agent for tailored recommendations

The real advantage emerges when you work with an independent agent who understands your specific operation rather than applying generic industry benchmarks. An independent agent will ask detailed questions about your customer traffic, product liability exposure, equipment value, and seasonal fluctuations-then recommend limits that prevent both overpaying and dangerous underpayment. For example, a professional services firm handling sensitive client data might prioritize higher Business Interruption limits to maintain payroll during recovery, while a contractor might emphasize off-site tool coverage and completed operations protection.

Coastal Huntington businesses face specific weather risks-nor’easters, hurricanes, and flooding-that demand adequate property limits and business interruption periods longer than inland competitors might need. An independent agent knows which carriers offer the most favorable terms for these regional exposures and which ones impose restrictive limitations. They’ll also identify coverage gaps: professional liability insurance for service providers, employment practices liability for businesses with multiple employees, or cyber liability for firms storing customer information. These decisions require local expertise and access to multiple carriers’ products, advantages that captive agents representing a single company simply cannot provide. When a claim occurs, your independent agent becomes your advocate, pushing for fair settlements and faster payouts rather than simply processing paperwork on the insurance company’s behalf.

Final Thoughts

A Business Owners Policy delivers the protection your Huntington business needs without the expense of buying three separate policies. Bundling General Liability, Commercial Property, and Business Interruption coverage reduces annual costs by 40 to 50 percent while eliminating dangerous gaps between carriers. The Hartford’s data shows that small business owners pay around $1,687 yearly for BOP coverage Huntington NY, a fraction of what separate policies would cost.

The real advantage emerges when you work with an independent agent who represents multiple top carriers. Unlike captive agents tied to a single company, independent agents shop your coverage across different insurers to find competitive rates and terms tailored to your actual operation. They understand local risks-coastal storms, flooding patterns, industry-specific exposures-and know which carriers offer the most favorable terms for Huntington businesses. When a claim happens, your independent agent advocates for fair settlements, coordinates between adjusters, and accelerates payouts rather than simply processing paperwork on the insurance company’s behalf.

We at JW Hirschfeld Agency, Inc. represent multiple top carriers and find tailored BOP solutions that fit your specific risks and budget. Whether you operate a retail shop, restaurant, contractor business, or professional services firm, we assess your exact exposure and recommend limits that prevent both overpaying and dangerous underpayment. Contact us today to discuss BOP coverage that protects your Huntington business at rates you can afford.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.