One accident on a job site can cost thousands in medical bills, property damage, and legal fees. Contractor general liability insurance protects your business from these financial disasters and is often required by clients and lenders.

We at JW Hirschfeld Agency, Inc. help builders understand what coverage they actually need and how to find the right policy at the right price. This guide walks you through the essentials.

What Contractor General Liability Insurance Actually Protects

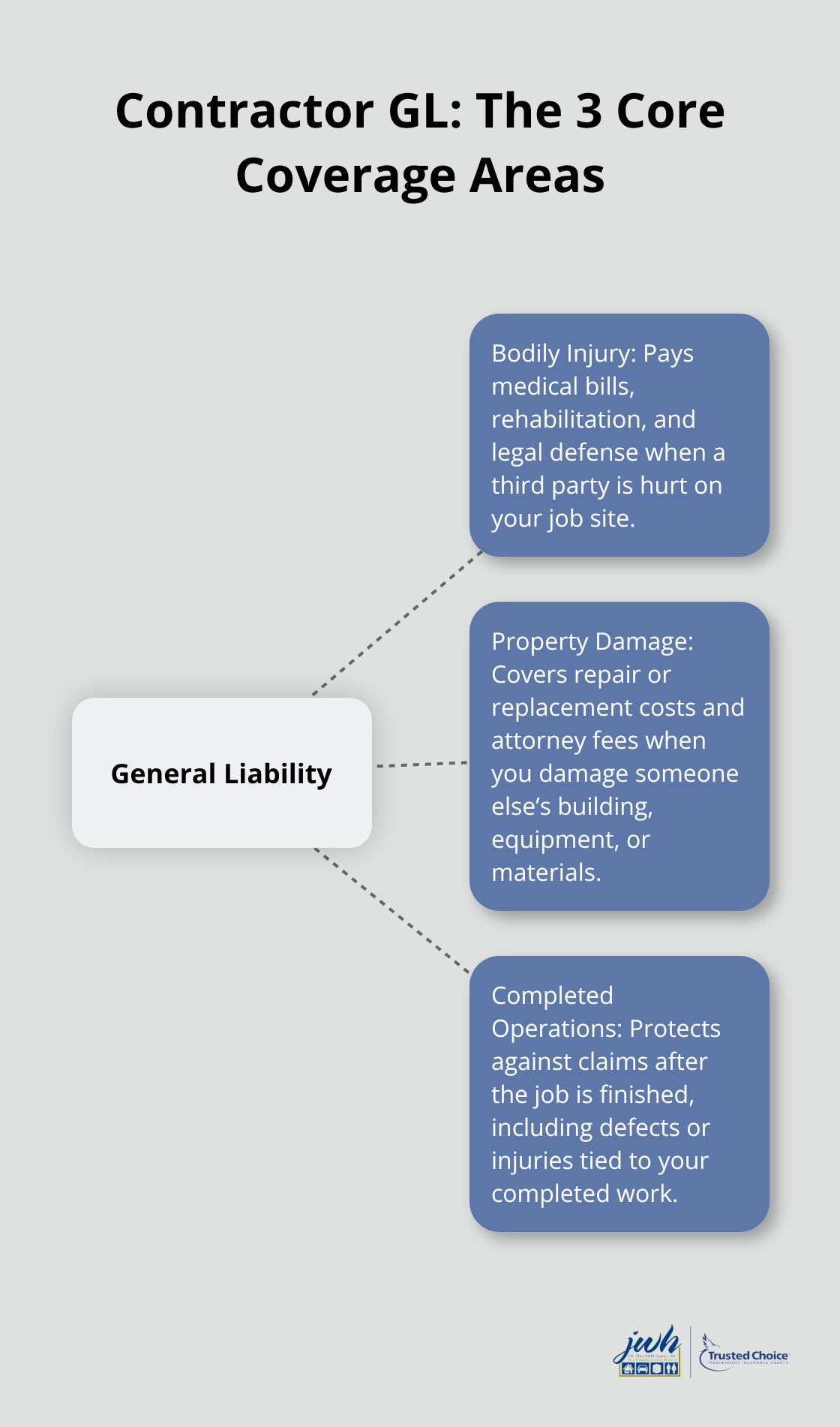

The Three Core Coverage Areas

General liability insurance protects your business across three main risk categories that directly impact your bottom line. First, bodily injury claims arise when a worker, client representative, or bystander gets hurt on your job site. Your policy covers medical bills, rehabilitation costs, and legal defense expenses if someone sues. Second, property damage to someone else’s building, equipment, or materials falls under GL protection. If your crew accidentally damages a client’s existing structure or a vehicle parked nearby, your policy pays for repairs, replacement, and legal fees. Third, completed operations liability protects you after project completion. If a homeowner discovers structural issues weeks later or sustains an injury from your finished work, GL provides coverage and legal defense.

Additional Coverage and Certificate Requirements

GL policies also cover personal and advertising injury claims like libel or copyright infringement, though these occur less frequently in construction work. Your policy typically includes a certificate of insurance (COI), which clients and lenders require before you start work. Many insurers now issue COIs online within hours, making contract compliance faster and smoother.

When something goes wrong, your insurer pays medical bills, repair costs, and attorney fees, keeping your business solvent when lawsuits arrive.

Understanding Premium Costs by Trade and Location

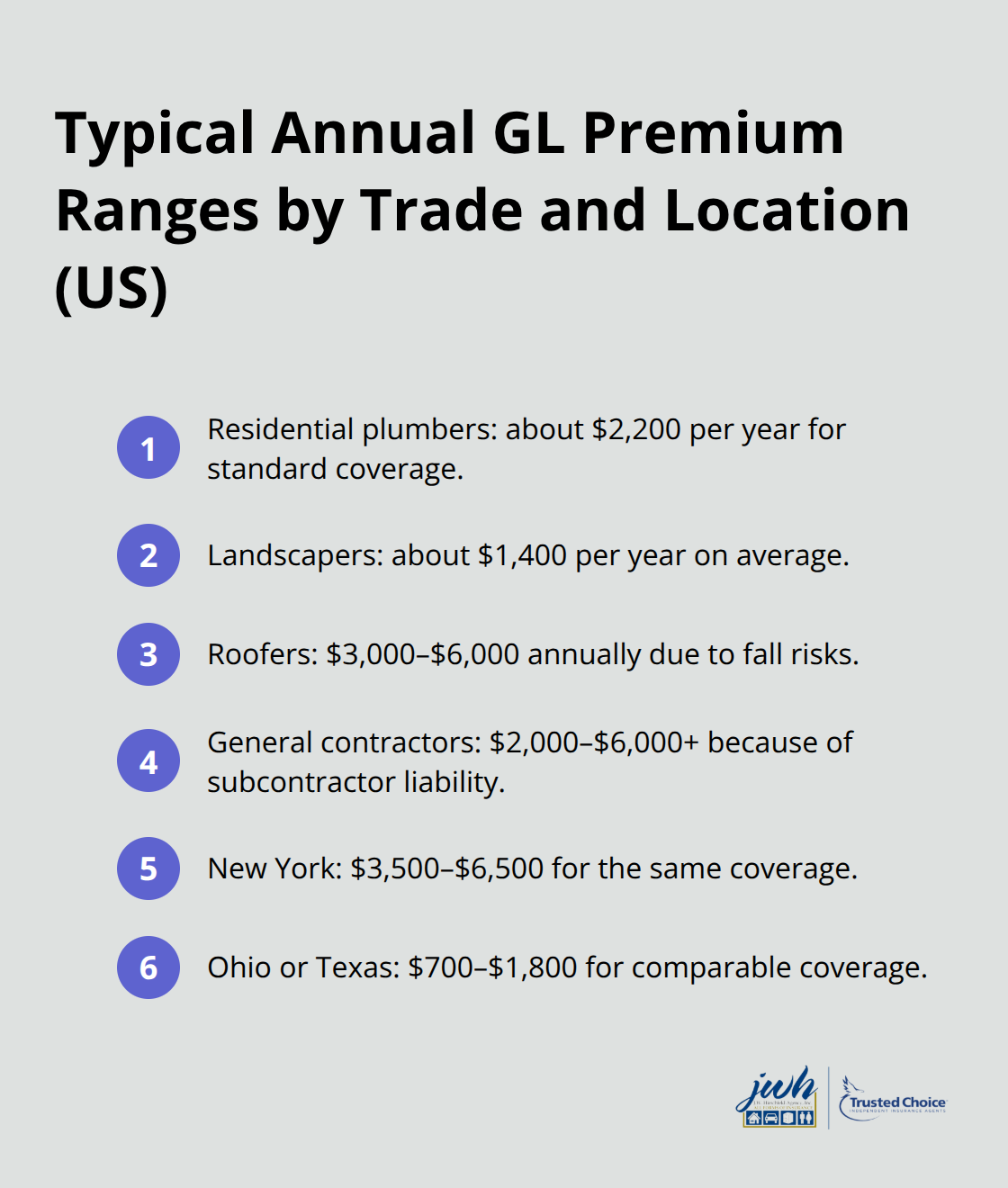

Cost varies significantly by trade and location. Residential plumbers pay roughly $2,200 annually for standard coverage, while landscapers average $1,400, according to Coverdash data cited by NerdWallet. Roofers typically run $3,000 to $6,000 annually because fall risks push premiums higher. General contractors often face $2,000 to $6,000 or more due to vicarious liability for subcontractors’ actions. Geography matters enormously-New York runs $3,500 to $6,500 annually for the same coverage that costs $700 to $1,800 in Ohio or Texas, reflecting stricter liability laws in some states.

Maximizing Value Through Carrier Comparison and Endorsements

An independent agent accesses multiple carriers and compares quotes side-by-side, showing you exactly what coverage differences justify any price gap. Agents identify endorsements that matter for your specific projects-like additional insured status for clients, which typically costs $0 to $150 per entity but protects you from disputes between project parties. This comparison process reveals which carriers offer the best fit for your risk profile and budget. The right endorsements can save you thousands in potential disputes while strengthening your contract position with clients and lenders.

Why Contractors Need General Liability Insurance

The True Cost of Being Uninsured

One lawsuit wipes out years of profit. A single accident where someone gets hurt on your job site or you damage a client’s property results in medical bills exceeding $100,000, property repairs running into the tens of thousands, and legal defense costs that mount regardless of whether you win or lose. General liability insurance helps cover the cost of accidents, property damage and bodily injury claims so your business survives the claim. Without it, you pay from your operating account, equipment reserves, or personal assets-a financial blow that most contractors cannot absorb.

Legal Requirements and Contract Mandates

In many states, general liability is legally required to bid on projects or secure financing. Lenders won’t fund a construction business without proof of coverage, and most clients won’t sign contracts without a certificate of insurance showing adequate limits. This isn’t optional-it’s a business requirement that blocks opportunities when you lack coverage. Clients demand COIs before work starts, and banks refuse loans to uninsured contractors. Without GL, you cannot compete for the projects that sustain your business.

Protecting Your Reputation and Personal Assets

GL protects your reputation when claims happen. Your insurer handles defense and settlement negotiations, not you. This keeps disputes from escalating into public conflicts that damage client relationships and referral networks. A contractor without GL coverage who faces a lawsuit becomes personally liable, which can destroy credit, force asset seizure, and end the business entirely. Your professional standing depends on having coverage that demonstrates financial responsibility to clients and lenders.

Premium Costs Reflect Your Trade and Risk Profile

General contractors commonly face GL premiums between $2,000 and $6,000 annually because they carry vicarious liability for subcontractors’ actions-meaning you’re responsible for injuries or damage caused by crews you hire. Roofers pay $3,000 to $6,000 yearly due to fall risks, while electricians typically run $1,000 to $2,000. These costs are investments in solvency, not expenses to minimize. An independent agent compares quotes across 25 to 40 carriers, identifying which ones price your specific trade and location most competitively. Agents also spot endorsements that matter-additional insured status for clients costs only $0 to $150 per entity but prevents disputes where you’re caught between competing parties on a project. Blanket additional insured endorsements typically run $100 to $500 yearly and automatically extend coverage to all clients, eliminating contract delays and approval friction.

Finding the Right Coverage Without Overpaying

Shopping independently ensures you’re not locked into one carrier’s rates or missing endorsements that strengthen your contract position and keep your business protected. An independent agent represents multiple top carriers and finds tailored coverage that fits your actual risk, not generic policies that overcharge or underprotect. This comparison process reveals which carriers offer the best fit for your risk profile and budget. The right endorsements can save you thousands in potential disputes while strengthening your contract position with clients and lenders. With proper GL coverage in place, you can now focus on selecting the right provider and policy limits that match your specific projects and growth plans.

How to Choose the Right Coverage and Provider

Document Your Specific Risk Profile

Start by writing down exactly what your crews do on job sites. General contractors managing multiple subcontractors face different risks than electricians working solo, and roofers confront fall hazards that framers don’t. List your typical projects, the number of employees, equipment values, and whether you regularly work in high-liability states like New York or California. This inventory becomes your foundation for accurate quotes and helps agents identify which carriers price your specific trade most competitively.

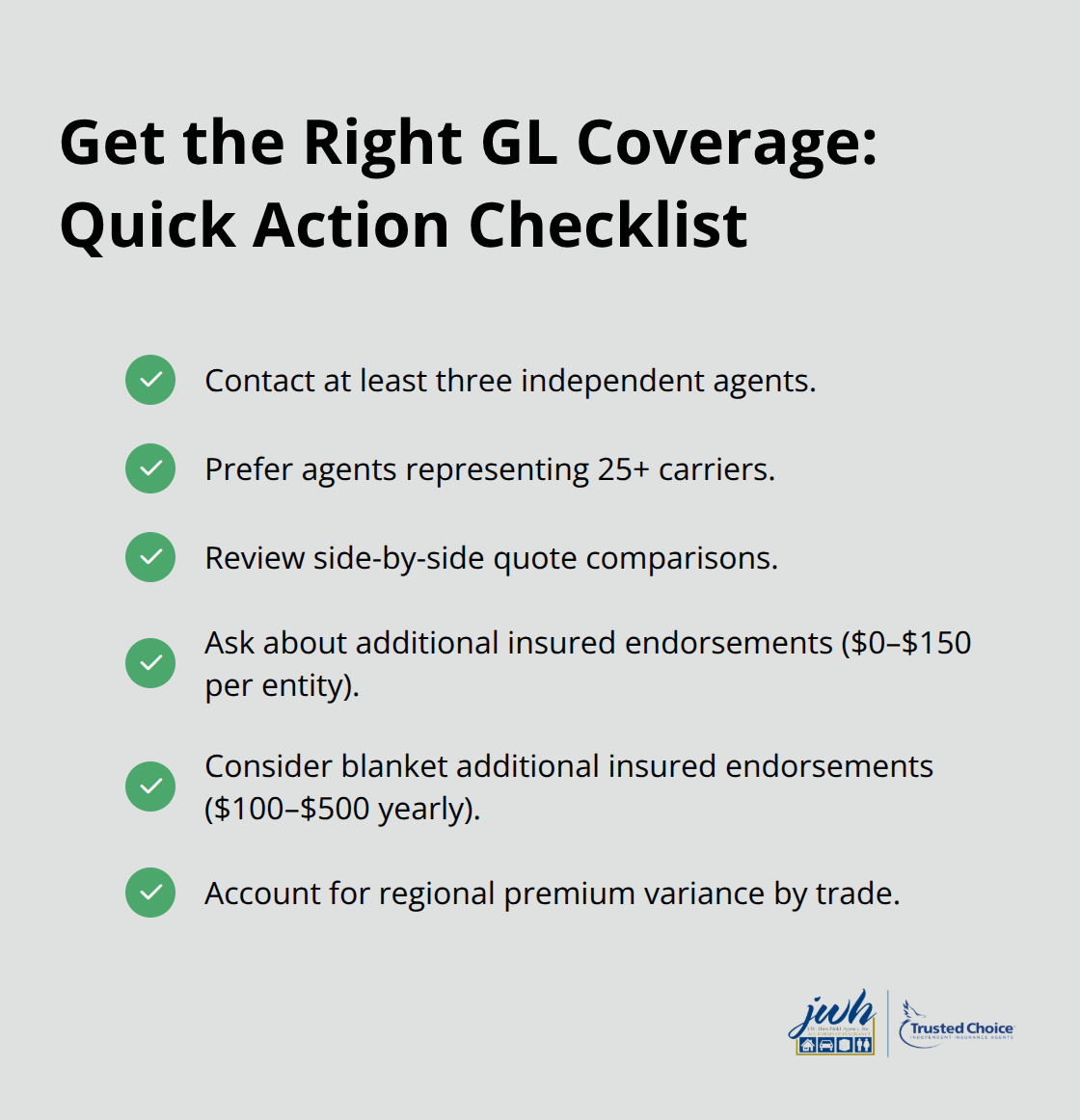

Request Quotes from Multiple Independent Agents

Contact at least three independent agents who represent 25 or more carriers. Independent agents access carriers that captive agents cannot reach, and they show you side-by-side comparisons revealing exactly which carriers price your specific trade and location most competitively. A roofer in Florida might find premiums ranging from $2,500 to $5,000 annually depending on the carrier, while the same roofer in Texas could pay $1,800 to $3,500. This variance matters enormously when multiplied across your business operations.

Ask each agent about additional insured endorsements, which cost $0 to $150 per entity and protect you when clients or lenders require coverage extension. Blanket additional insured endorsements typically cost $100 to $500 yearly and automatically add all current and future clients to your policy, eliminating contract delays.

Select Policy Limits That Match Your Project Scope

Policy limits determine how much your insurer pays before you cover the rest. Standard contractor general liability insurance policy limits run $1 million per occurrence and $2 million aggregate for small to mid-sized contractors, costing roughly $750 to $2,500 annually. Larger general contractors managing $5 million-plus projects often need $2 million per occurrence and $4 million aggregate, pushing premiums to $3,000 to $6,000 or higher. Higher limits cost more upfront but protect you if a single accident exceeds standard coverage. Try selecting limits that match your largest typical project value plus a 20 percent cushion.

Balance Deductibles with Cash Flow Needs

Deductibles work inversely to premiums-selecting $1,000 deductibles instead of $500 reduces your annual premium roughly 10 to 15 percent, but you pay more out-of-pocket when claims occur. Most contractors find $500 to $1,000 deductibles reasonable for cash flow management. An independent agent helps you align limits and deductibles with actual project scope rather than generic minimums, protecting you without overpaying for unnecessary coverage.

Leverage Annual Policy Reviews for Better Rates

An independent agent monitors your policy annually, catching endorsement gaps and re-shopping coverage at renewal to capture price drops across carriers-a service that captive agents tied to single carriers simply cannot provide. This ongoing advocacy means you stay competitive on pricing as your business grows and market conditions shift. Getting professional advice from a local insurance agency ensures you receive guidance tailored to your contractor business rather than generic recommendations.

Final Thoughts

Contractor general liability insurance protects your business from the financial devastation that follows accidents on job sites. Medical bills, property damage claims, and legal defense costs drain operating accounts and force contractors into personal liability without proper coverage. Standard limits of $1 million per occurrence and $2 million aggregate work for most small to mid-sized contractors, though larger projects demand higher protection based on your actual project values and risk exposure.

Independent agents represent 25 to 40 carriers and show you exactly which options fit your specific trade, location, and budget through side-by-side quote comparisons. They identify endorsements like additional insured status that strengthen your contract position with clients and lenders, and they re-shop your coverage at renewal to capture price drops as market conditions shift. During claims, they act as your advocate with the insurer, pushing for timely resolution rather than leaving you to navigate disputes alone.

Contact JW Hirschfeld Agency, Inc. or another independent agent in your area to request quotes that show policy limits, deductibles, and endorsement costs. Document your typical projects, crew size, and equipment values so agents can match you with carriers that price your specific trade most competitively. Select limits matching your largest typical project plus a safety margin, and schedule annual reviews to catch coverage gaps as your business grows.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.