Owning rental properties comes with real financial exposure. Tenants can cause damage, accidents happen on your property, and lost rent can devastate your cash flow-none of which standard homeowners policies cover.

A landlord insurance policy fills those gaps with targeted protection for your investment. We at JW Hirschfeld Agency, Inc. help property owners understand exactly what coverage they need and how to avoid costly mistakes when choosing a plan.

What Landlord Insurance Actually Covers

Core Coverage That Protects Your Investment

Landlord insurance protects the structure of your rental property and your liability exposure-two things standard homeowners policies explicitly exclude. The core coverage includes the dwelling itself (the building structure and attached systems), premises liability (legal defense and medical costs if someone is injured on your property), and fair rental value coverage that replaces lost rent when your property becomes uninhabitable due to a covered loss like fire or severe weather. Many policies also include wind and hail protection, which matters significantly in regions prone to storms. You can add optional coverage for water backup, legal expenses, and rent guarantee protection if a tenant defaults.

Understanding the Cost Structure

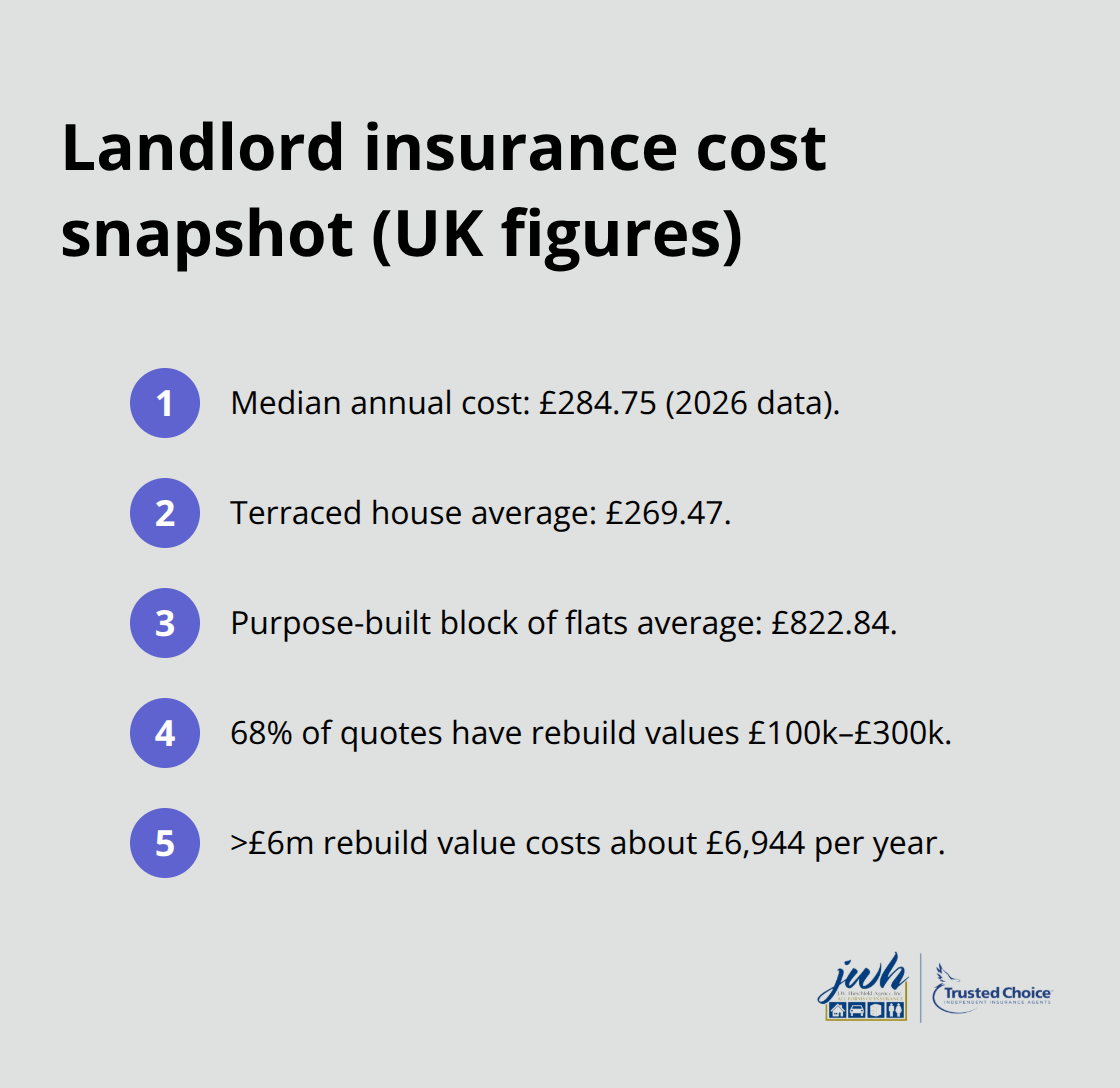

The median UK landlord insurance cost sits around £284.75 annually according to Alan Boswell Group data from 2026, though this varies dramatically by property type, location, and rebuild value. A terraced house averages £269.47, while a purpose-built block of flats jumps to £822.84. Rebuild value drives costs more than anything else-properties valued at £100,000 to £300,000 represent 68% of quotes, while properties exceeding £6 million in rebuild value cost around £6,944 per year.

Why Standard Homeowners Policies Fall Short

The real reason landlords need separate coverage comes down to what homeowners policies exclude. Standard homeowners insurance treats your rental property as an investment, not a residence, and denies claims related to tenant damage, loss of rental income, and liability from rental activities. Landlord insurance is designed to protect your income and the insured property in the event of tenant-related damages, certain disasters and liability claims. If a tenant accidentally starts a kitchen fire that makes the unit unlivable for three months, your homeowners policy covers the structural damage but not the £3,000 in rent you lose during repairs-landlord insurance fills exactly that gap.

How Tenant Type and Location Affect Your Premium

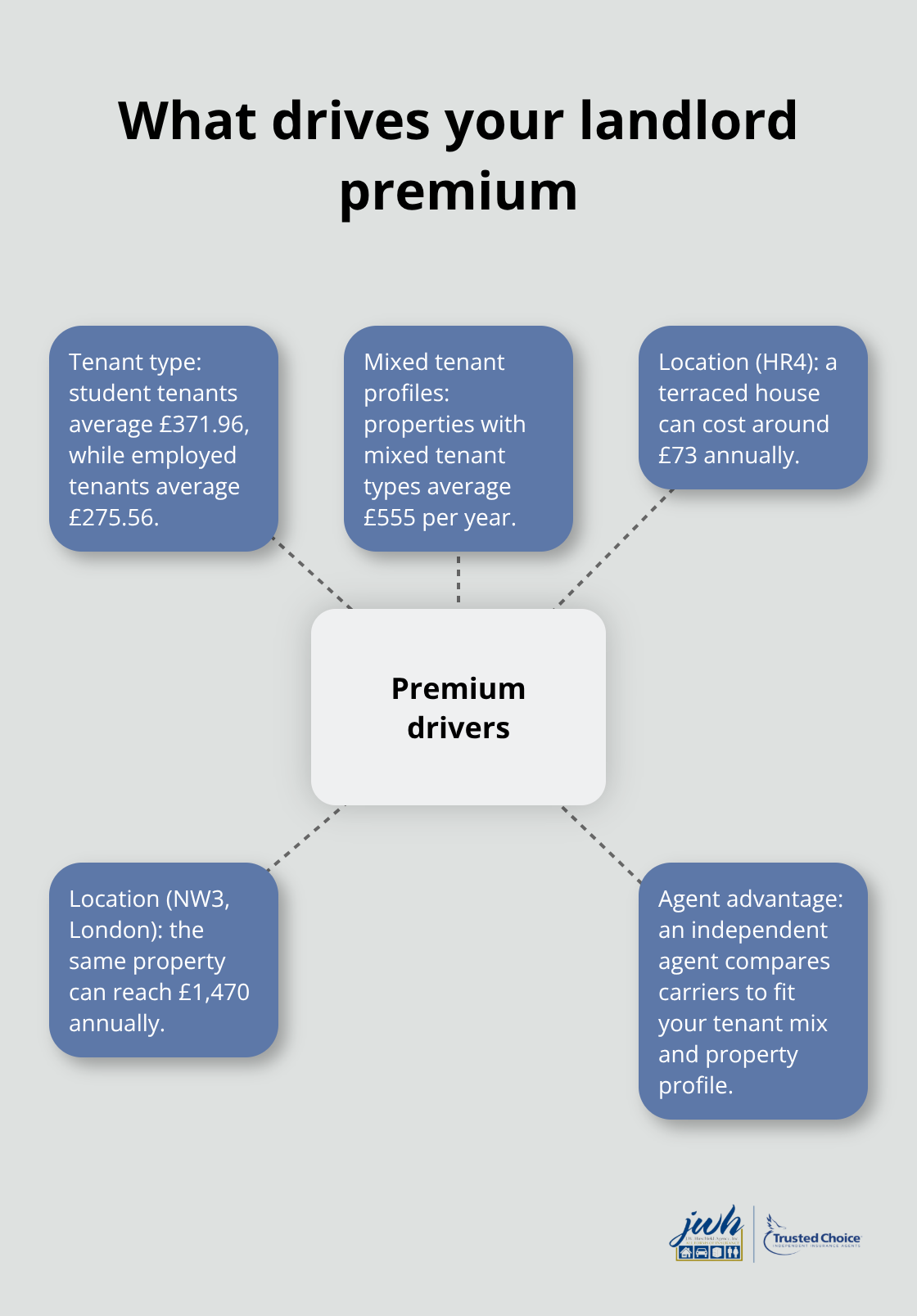

Tenant type affects your premium significantly: student tenants average £371.96 annually while employed tenants cost £275.56, according to Alan Boswell Group. Properties with mixed tenant types jump to £555. Regional variation is pronounced too-a terraced house in postal code HR4 costs around £73 annually while the same property in NW3 (London) reaches £1,470.

An independent agent compares carriers and customizes coverage to your specific tenant mix and property profile rather than accepting a one-size-fits-all quote online, which matters when your premium can swing by nearly £1,400 based on location alone.

Common Gaps in Standard Homeowners Policies

Loss of Rent Coverage Exclusions

Your homeowners policy treats your rental property as an investment property, not a residence, and that distinction creates three massive coverage gaps that leave landlords financially exposed. The first gap is loss of rent coverage. If a fire, severe storm, or other covered event makes your rental unit uninhabitable, your homeowners policy pays for the structural repairs but refuses to cover the rental income you lose while the property sits empty during reconstruction. Loss of rent coverage applies only when repairs are needed due to a covered peril, such as fire or storm damage-not for vacancies or tenant turnover. Landlord insurance fills this gap with fair rental value coverage that pays your lost income during the repair period, protecting your cash flow when you need it most.

Liability Limits for Rental Properties

The second gap involves liability limits designed for owner-occupied homes, not rental properties where you face greater exposure. Your homeowners liability coverage typically maxes out at £300,000 to £500,000, but a serious injury on your rental property-a maintenance worker hurt on the stairs, a visitor slipping in the lobby-can generate legal costs and settlements well beyond those limits. Landlord policies specifically address rental liability with higher limits and coverage for incidents involving tenants, contractors, and third parties. This protection matters because your exposure multiplies when strangers regularly access your property.

Damage from Tenant Actions Not Covered

The third and most costly gap involves tenant-caused damage. If a tenant accidentally starts a kitchen fire, causes significant water damage through negligence, or damages systems and fixtures, your homeowners policy denies the claim because it excludes damage caused by occupants of the insured property. Landlord insurance covers these tenant-related damages to the building structure and systems, protecting your investment from the wear and tear that comes with renting. An independent agent reviews your property profile, asks about your tenant type and lease terms, and builds a customized policy that actually covers what you need rather than leaving you with expensive surprises when a claim lands on your desk.

Why Coverage Language Matters More Than You Think

Different carriers handle these three gaps in dramatically different ways. One carrier might include tenant damage under dwelling coverage while another excludes it entirely. One might cap fair rental value at six months while another extends it to twelve. An online quote tool cannot navigate these nuances or explain how each gap affects your specific property and tenant situation. An independent agent reviews your property profile, asks about your tenant type and lease terms, and builds a customized policy that actually covers what you need rather than leaving you with expensive surprises when a claim lands on your desk. This is where the right partnership makes the difference between adequate protection and financial exposure.

How to Choose the Right Landlord Insurance Policy

Calculate Your Rebuild Value Accurately

Start with your actual rebuild value, not your property’s market price. Rebuild value represents what it costs to reconstruct your building from scratch if it burns to the ground, and it drives your entire premium. You can determine your rebuild value using an online calculator or by contacting a local contractor. Once you have this figure, your premium becomes predictable. A property with a £150,000 rebuild value costs substantially less than one valued at £500,000, but getting the number wrong means either overpaying for coverage you don’t need or facing a massive shortfall when disaster strikes.

Match Coverage to Your Tenant Profile

Document your tenant situation honestly. Student tenants cost £371.96 annually on average while employed tenants average £275.56, according to Alan Boswell Group research from 2026. Mixed-tenant properties jump to £555 per year because carriers view portfolio diversity as higher risk. An independent agent asks the right questions about your tenant mix and lease terms, then shops multiple carriers to find one that prices your specific situation fairly rather than forcing you into a generic profile that doesn’t fit.

Account for Regional Location Differences

Regional location matters as much as property type. A terraced house in postal code HR4 costs around £73 annually while an identical property in London’s NW3 postal code reaches £1,470-nearly a twentyfold difference driven by local claims history, construction costs, and weather patterns. This variation means online quote tools that don’t account for your specific street or neighborhood give you false confidence in pricing. An independent agent knows your local market, understands which carriers price fairly in your area, and can explain why premiums vary so dramatically.

Select Optional Coverage Based on Property Risk

On optional coverage, rent guarantee and rent default protection typically add around £195 annually, while legal expenses coverage with £50,000 protection adds £60 to £80. Water backup coverage availability varies by region and can meaningfully impact your total premium. Rather than guessing which extras you need, an independent agent reviews your property’s specific risks (whether you’re in a flood-prone area, whether your building has aging plumbing, whether you’ve experienced tenant defaults before) and recommends coverage that actually protects you.

Leverage Bundle Discounts for Maximum Savings

Bundle discounts through an independent agent compound these savings significantly. Insuring your landlord property alongside your personal auto or home policy through the same broker yields measurable savings compared to splitting coverage across multiple carriers, and adding renters, RV, or boat policies extends those discounts further. This bundling approach simplifies your administration and strengthens your relationship with someone who knows your complete risk profile.

Final Thoughts

Landlord insurance protects what standard homeowners policies ignore: your rental income, your liability exposure, and damage caused by tenants. A three-month vacancy from fire damage costs thousands in lost rent, a serious injury on your property generates legal bills that exceed standard liability limits, and tenant-caused damage to plumbing or electrical systems drains your reserves fast. A landlord insurance policy fills these gaps with targeted protection designed specifically for rental properties.

Getting the right coverage means matching your policy to your actual property and tenant situation, not accepting a generic online quote. Your rebuild value, tenant type, location, and optional coverage needs are unique to your investment, and regional variation alone can swing your premium by £1,400 or more. Student tenants cost significantly more than employed tenants, purpose-built blocks of flats cost nearly three times what terraced houses cost, and these differences determine whether you pay fairly or overpay for coverage that doesn’t fit.

We at JW Hirschfeld Agency, Inc. represent multiple top carriers and shop your specific situation across all of them rather than steering you toward one company’s standard product. We ask the right questions about your property, your tenants, and your risk tolerance, then build a customized landlord insurance policy that actually protects you and bundle your coverage with auto, home, and other policies to save money you won’t find buying separately. Contact us today for a quote that fits your property and your budget.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.