Long Island homeowners face distinct insurance challenges that standard policies simply don’t address. Coastal weather patterns, salt spray damage, and hurricane exposure create risks that generic coverage overlooks.

At JW Hirschfeld Agency, Inc., we know that Long Island homeowners insurance works best when it’s built around your specific property and lifestyle. This blog post shows you how to customize your coverage to match what actually matters for your home.

Why Standard Policies Miss Long Island’s Real Risks

Standard homeowners policies treat all properties the same, which works fine for homes in stable climates but fails spectacularly on Long Island. Your coastal location creates exposures that generic coverage simply ignores. Hurricane-force winds, salt spray corrosion, nor’easters, and freeze-thaw cycles damage homes differently here than they do inland. A policy written for suburban Pennsylvania won’t protect you from the specific threats your Long Island home faces every season. Most carriers writing standard HO-3 policies don’t account for the elevated risk of water intrusion from coastal storms, roof damage from salt-laden winds, or the accelerated deterioration of exterior materials that comes with proximity to the ocean. Claims denials reveal coverage gaps that should have been addressed from the start.

High-Value Homes Need More Than Basic Protection

If your home contains valuable items-jewelry, art, antiques, or collections-standard policies cap personal property coverage at 50 to 70 percent of your dwelling limit. That means a $500,000 home gets roughly $250,000 to $350,000 in personal property coverage, far less than what your belongings are actually worth. Endorsements fix this problem, but only if you request them and document what you own. Independent agents access multiple carriers to find policies that let you schedule high-value items separately, ensuring full replacement cost without arbitrary caps. A single loss-whether from theft, fire, or weather-leaves you significantly underinsured without proper endorsements.

One-Size-Fits-All Coverage Ignores Your Lifestyle

Rental income from a guest house, a home-based business, or income-generating hobbies require additional liability and property coverage that standard policies exclude. A homeowner who rents out a room or runs a consulting business from their home faces liability exposure that a typical HO-3 doesn’t cover. Likewise, if you own a second property on Long Island or nearby, you need separate coverage tailored to that specific risk. Generic policies force you to choose between accepting inadequate coverage or paying for options you don’t need.

Why Independent Agents Solve the Personalization Problem

Local independent agents understand Long Island’s mix of residential, coastal, and mixed-use properties and customize coverage to match your actual situation rather than pushing unnecessary add-ons or leaving you underprotected. An independent broker representing multiple top carriers finds tailored coverage and competitive pricing that aligns with your specific exposures. This hands-on approach means your policy reflects your home, your belongings, and your lifestyle-not a template designed for everywhere and nowhere.

How to Spot What Your Long Island Home Actually Needs

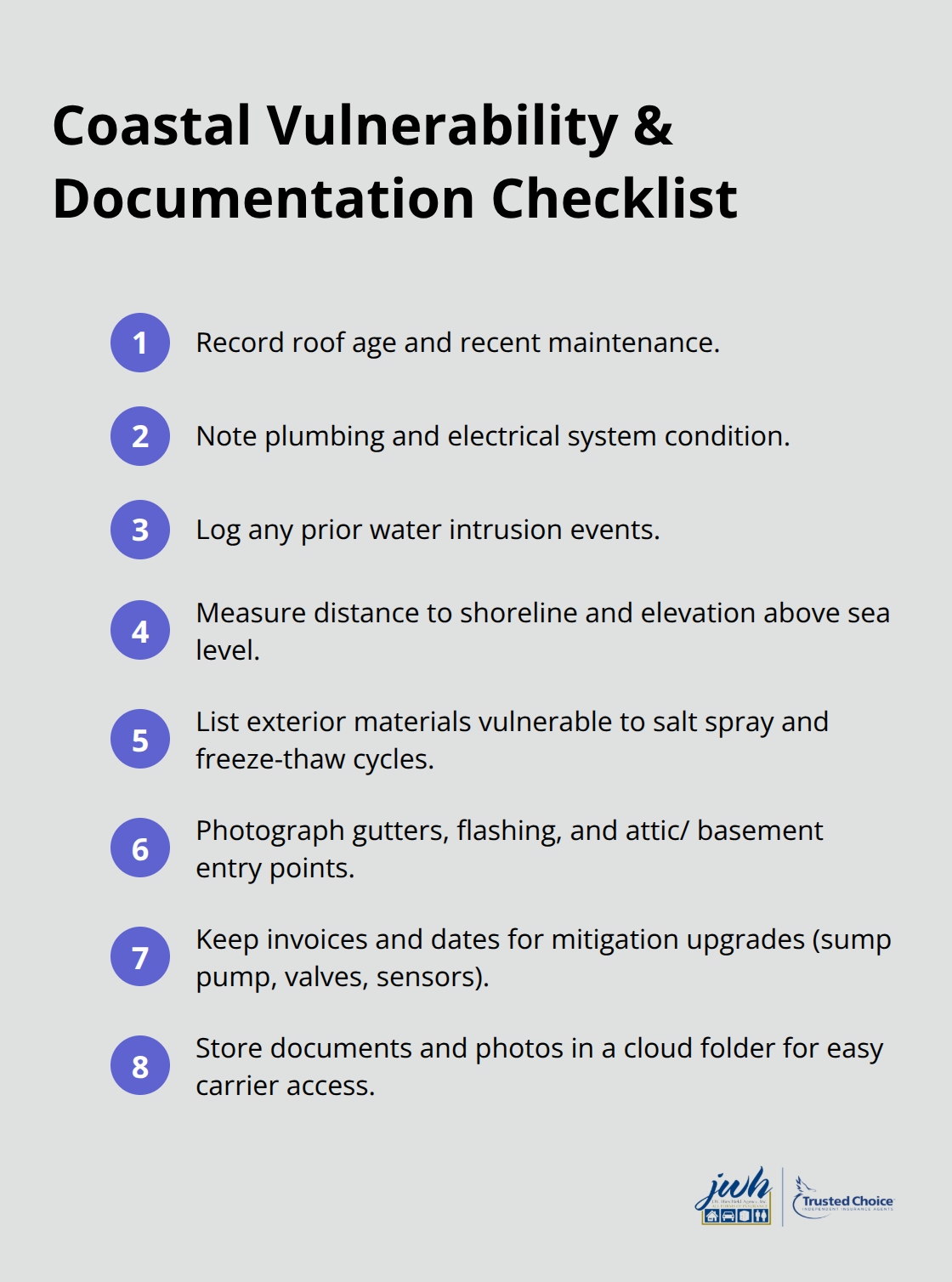

Assess Your Property’s Coastal Vulnerabilities

Walk your property and catalog what’s actually at risk. Coastal homes need different protection than inland properties, and your policy should reflect that reality. Salt spray corrodes metal roofing and gutters faster than inland wear; freeze-thaw cycles crack foundations and burst pipes; nor’easters drive water into attics and basements through gaps that wouldn’t matter elsewhere.

Document your roof’s age, the condition of your plumbing and electrical systems, and whether you’ve had water intrusion before. Insurance carriers ask for these details because they directly affect your coverage needs and pricing. If you’ve experienced even minor water damage, that history shapes what endorsements make sense for your next policy.

Homes within one mile of the south shore or within 2,500 feet of the north shore face higher coastal storm exposure, which may push you toward NYPIUA Basic or Broad Form coverage paired with voluntary-market wrap-around policies that add liability, personal property, and theft protection. The Coastal Market Assistance Program through NYPIUA helps homeowners in these zones find coverage when standard carriers decline them, combining NYPIUA’s foundational protection with voluntary-market endorsements for comprehensive coverage.

Schedule High-Value Items Separately

Personal property coverage under a typical HO-3 maxes out at 50 to 70 percent of your dwelling limit, which means jewelry, art, antiques, and collections are dramatically underinsured unless you schedule them separately. Scheduled personal property endorsements list each item with its replacement cost, eliminating depreciation and coverage caps.

High-value items and income-generating activities require specific endorsements that standard policies either exclude or severely limit. An independent agent accesses carriers that write endorsements for these situations-home business liability, rental income coverage, and secondary property protection-rather than forcing you to accept inadequate coverage or overpay for unnecessary options.

Leverage Discounts and Deductible Strategies

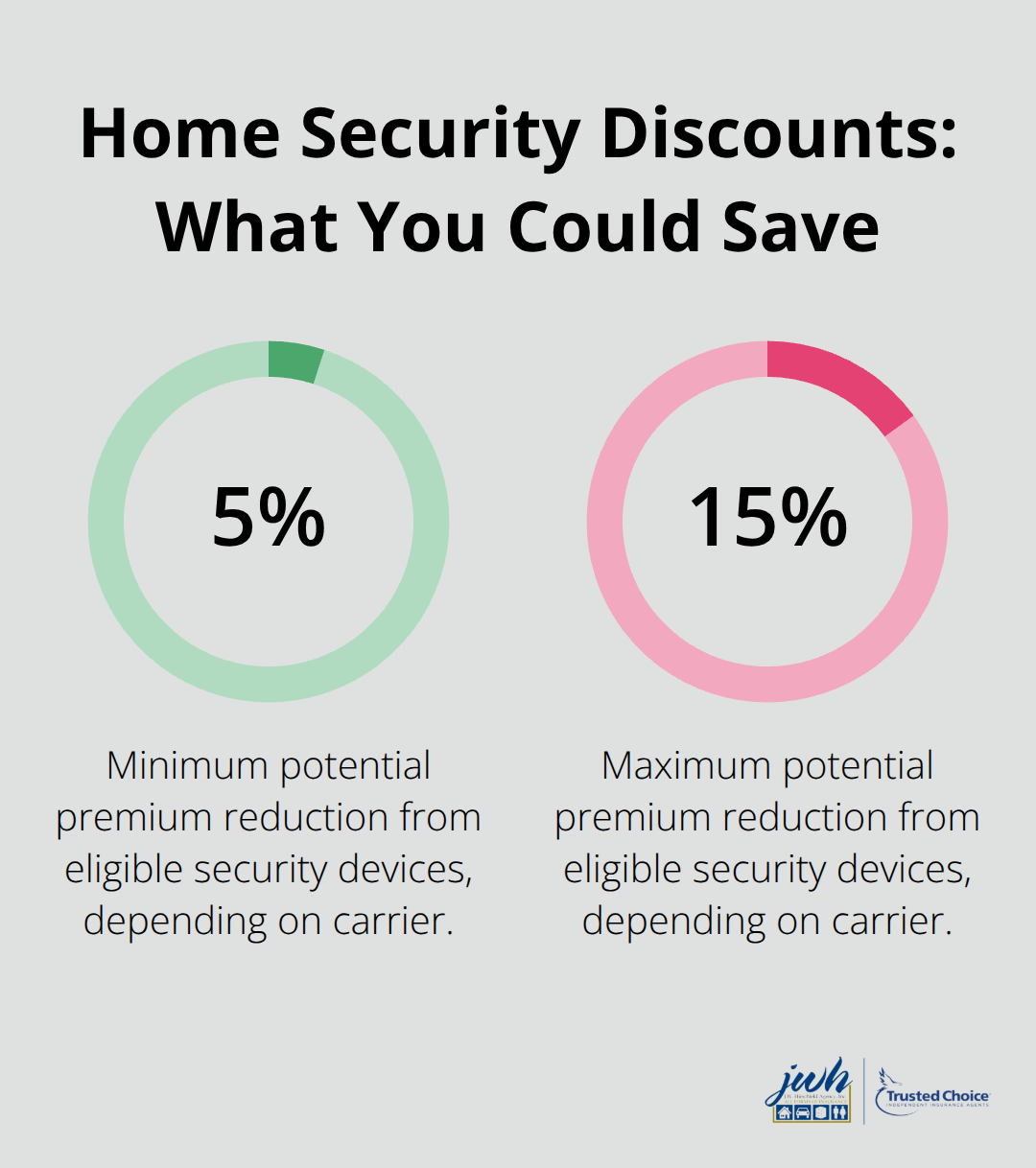

Bundling auto and home coverage across multiple carriers yields multi-policy discounts that direct online quotes often miss because they’re limited to a single company’s products. Installing security systems, deadbolts, and smoke detectors qualifies for discounts that reduce premiums by 5 to 15 percent depending on your carrier and equipment type.

Raising your deductible from $500 to $1,000 lowers annual premiums by roughly 10 to 15 percent, but only if you have emergency savings to cover that higher out-of-pocket cost. An independent broker representing multiple top carriers finds the combination of endorsements, discounts, and deductible levels that matches your home, your budget, and your risk tolerance.

These personalized adjustments form the foundation of a policy that actually protects what matters. The next step involves understanding how an independent agent transforms this assessment into comprehensive coverage that adapts as your life and property change.

Why Independent Agents Win at Personalization

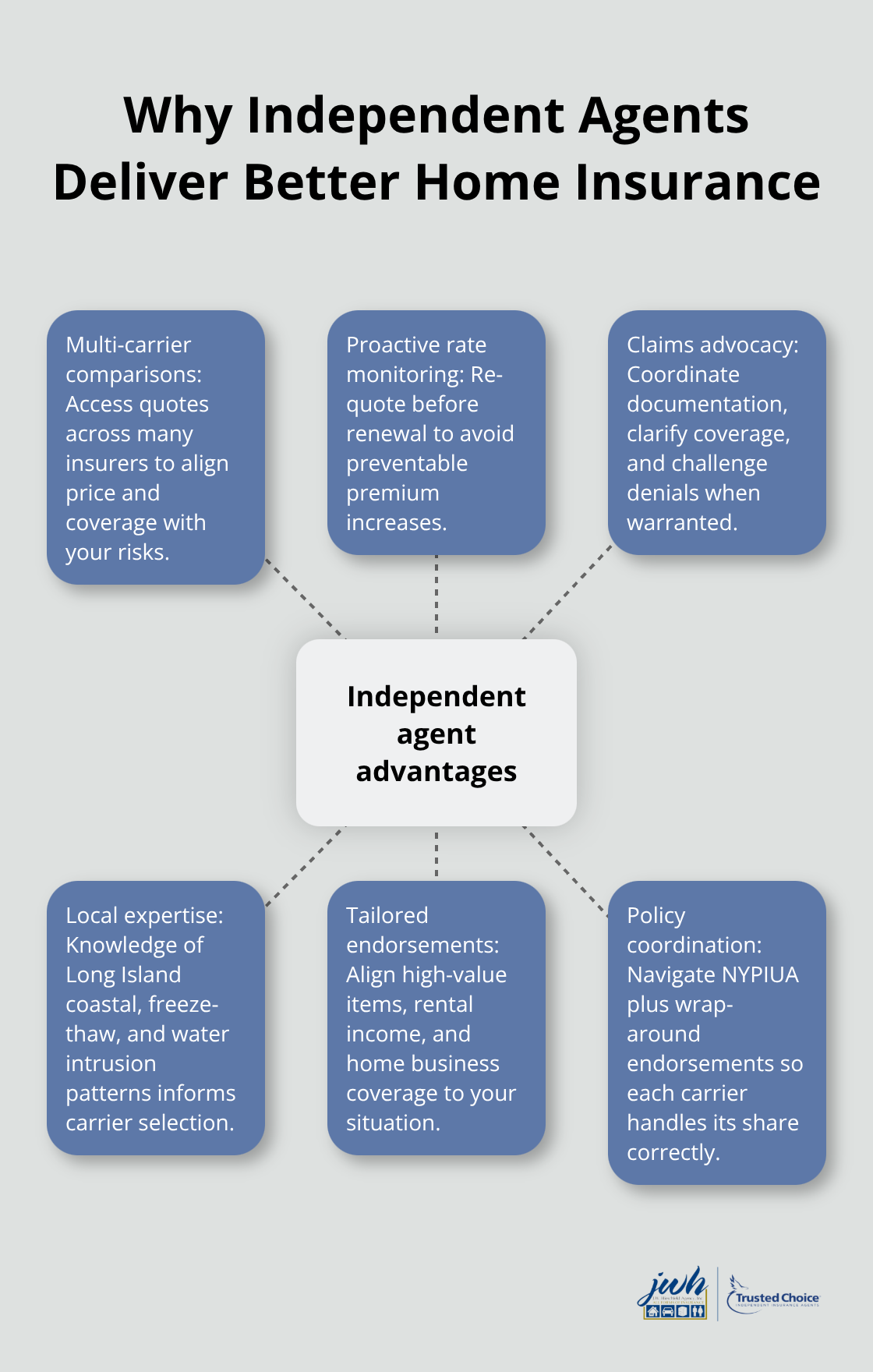

Multiple Carriers Mean Real Comparison Shopping

When you shop for homeowners insurance online, you’re confined to one company’s products and pricing. Direct carriers like Progressive or State Farm control what you see, what you can customize, and what discounts apply. Independent agents operate differently. We at JW Hirschfeld Agency, Inc. represent multiple top carriers, which means we can compare actual quotes across different companies instead of showing you one option and calling it competitive.

A homeowner in Huntington might find that Carrier A offers better rates for a coastal property with a new roof, while Carrier B provides superior coverage for scheduled jewelry at a lower premium. You don’t see that comparison online-you see whatever one carrier decides to show you. The difference matters: independent brokers representing 20+ carriers uncover pricing and coverage combinations that direct-to-consumer sites simply cannot access.

Proactive Rate Monitoring Protects Your Budget

When rates rise, a good independent agent monitors your premium and re-quotes across multiple carriers to find savings before your renewal notice arrives. Direct carriers tell you your new rate; independent agents find you a better one. This proactive approach means you don’t accept premium increases that other carriers would undercut.

Claims Support That Actually Works for You

Claims are where the real advantage emerges. When water damage or a winter storm hits your Long Island home, you need someone fighting for you, not a chatbot explaining policy terms. Independent agents act as liaisons with your carrier, translating coverage details, submitting documentation, and pushing back on denials that shouldn’t stand.

If your NYPIUA Basic Form policy pairs with a voluntary-market wrap-around endorsement, claims become more complex-different carriers may handle different parts of your loss, and coordination matters. An agent familiar with your specific policy structure navigates that complexity and ensures each carrier pays their portion. Direct carriers have licensed representatives available, but they work for the insurer, not for you. An independent agent works for you. That distinction determines whether a claim gets resolved fairly or whether you spend months fighting for coverage you thought you had.

Local Expertise Prevents Costly Coverage Mistakes

Long Island’s coastal exposure, freeze-thaw cycles, and water intrusion patterns are distinct from inland risks, and carriers price accordingly. An agent with deep experience serving Nassau and Suffolk counties knows which carriers understand coastal risk, which ones deny mold claims unnecessarily, and which ones cover secondary properties or rental income without overcharging. That knowledge prevents you from buying inadequate coverage or overpaying for unnecessary add-ons. You get a policy that reflects Long Island reality, not a generic template adjusted for your zip code.

Final Thoughts

Customized Long Island homeowners insurance protects what actually matters to you, not what a generic template assumes you need. The gap between standard coverage and your real exposures costs money at claim time, when denials arrive and you discover your policy doesn’t cover the damage you thought it did. Coastal weather, high-value belongings, and lifestyle-specific risks demand a policy built around your property and circumstances, not around what carriers find easiest to sell.

Working with a local independent agent eliminates the guesswork. Instead of accepting whatever one carrier offers online, you access multiple top carriers and the expertise to match each one’s strengths to your specific situation. An independent broker representing 20+ insurers finds rate combinations, endorsement options, and discount strategies that direct-to-consumer sites cannot access, and when a claim happens, you have someone fighting for you rather than a company explaining why coverage doesn’t apply.

Your next step is straightforward: reach out to JW Hirschfeld Agency, Inc. for a personalized quote that reflects your home’s actual value, your belongings, and your Long Island location. A conversation with an independent agent takes minutes and reveals coverage options and savings you won’t find online. Protect your home properly, starting today.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.