Running a construction business in New York means navigating strict insurance requirements. Without the right contractor insurance policy in place, you risk hefty fines, license suspension, and serious financial exposure on every project.

We at JW Hirschfeld Agency, Inc. help builders understand exactly what coverage they need and how to get it at the best rates. This guide breaks down NY’s mandatory requirements, explains each coverage type, and shows you how to pick a policy that actually protects your business.

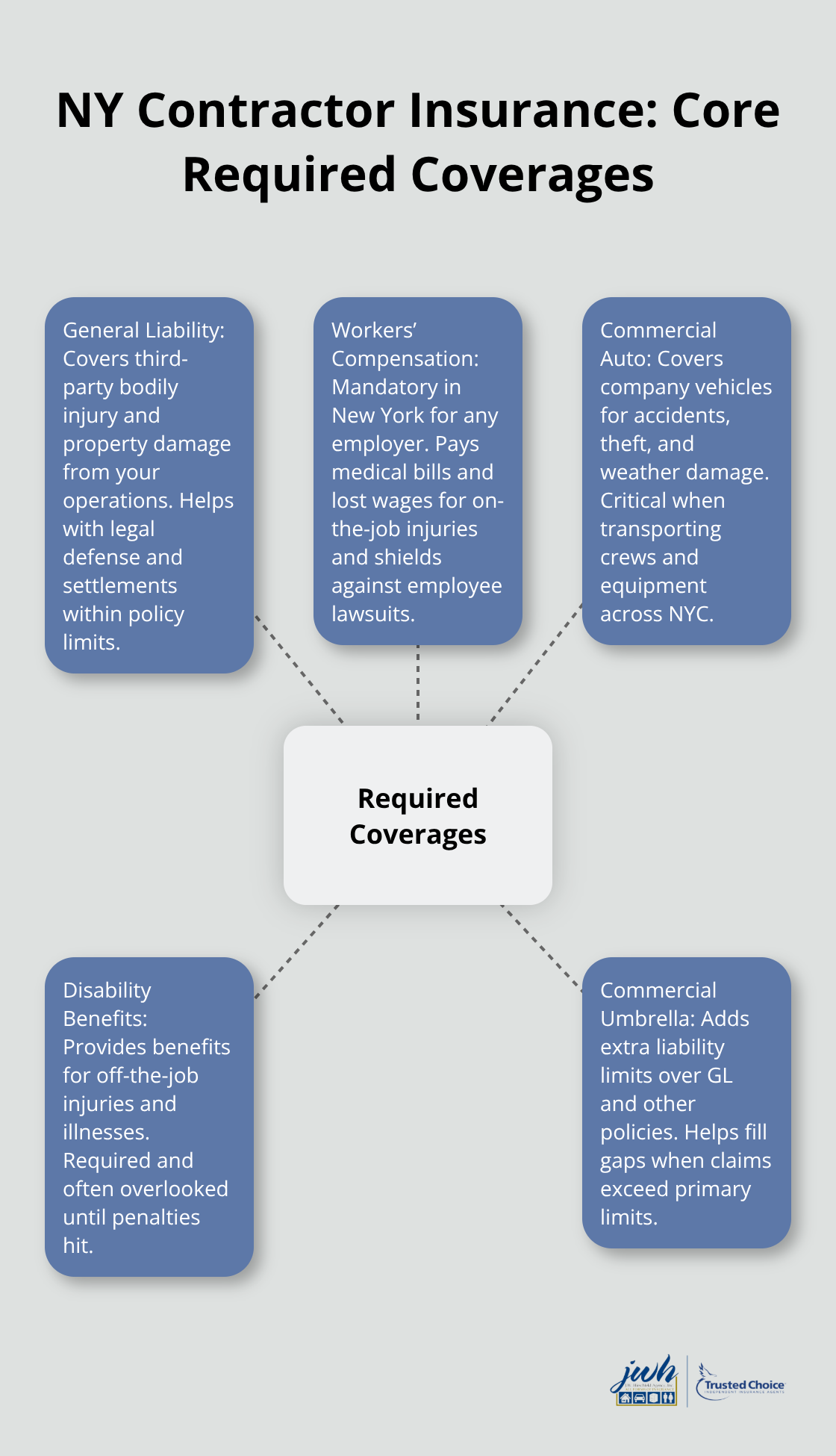

What NY Actually Requires From Contractors

New York’s insurance mandates aren’t suggestions-they’re legal obligations tied directly to your license and your ability to operate. General Liability Insurance, Workers’ Compensation Insurance, Commercial Auto Insurance, and Disability Benefits Insurance form the foundation of what the state requires. General Liability covers bodily injury and property damage claims from your operations, protecting you when someone is injured at a job site or your work damages client property. Workers’ Compensation is mandatory in New York and covers medical costs and lost wages for employees injured on the job-it also shields your company from lawsuits by employees. Commercial Auto Insurance covers vehicle-related losses including accidents, theft, and weather damage, which matters significantly when you transport equipment and crews across NYC’s congested streets. Disability Benefits Insurance covers off-the-job injuries and illnesses, a requirement many contractors overlook until they face penalties.

The New York Industrial Code holds you fully liable for damages caused by negligent acts of your employees or subcontractors, meaning basic liability coverage often isn’t enough. This reality is why supplemental policies like Commercial Umbrella Insurance exist-they provide additional liability limits beyond your general liability and workers’ compensation coverage, filling gaps that standard policies leave exposed.

Why Minimum Coverage Falls Short

Standard policies frequently leave dangerous gaps, especially on high-risk projects. The New York Scaffold Law (Labor Law §240/241) provides strict liability for falls from heights and falling objects, directly influencing the coverage limits you actually need. High-rise work, tower crane operations, and projects involving historic properties require higher coverage levels than what standard policies typically offer. Historic properties in NYC require Landmarks Preservation Commission permits, and non-compliance triggers heavy fines that your insurance won’t cover. Builder’s Risk Insurance protects buildings under construction against vandalism, theft, fire, explosions, hail, and lightning-essential for projects lasting weeks or months. Professional Liability Insurance covers defense costs and damages from professional errors or missed deadlines, protecting your reputation and finances.

How an Independent Agent Identifies Your Coverage Gaps

An independent insurance agent who understands New York construction identifies which gaps apply to your specific work and recommends endorsements or layered coverage before you face a claim denial. Unlike captive agents tied to one carrier, independent brokers representing multiple top carriers assess your operations across different insurers and find the combination that actually protects your business. This approach matters because your project type, crew size, and job location all shift what you truly need versus what a standard policy offers.

What Each Coverage Type Actually Protects

Workers’ Compensation: Mandatory Protection for Your Crew

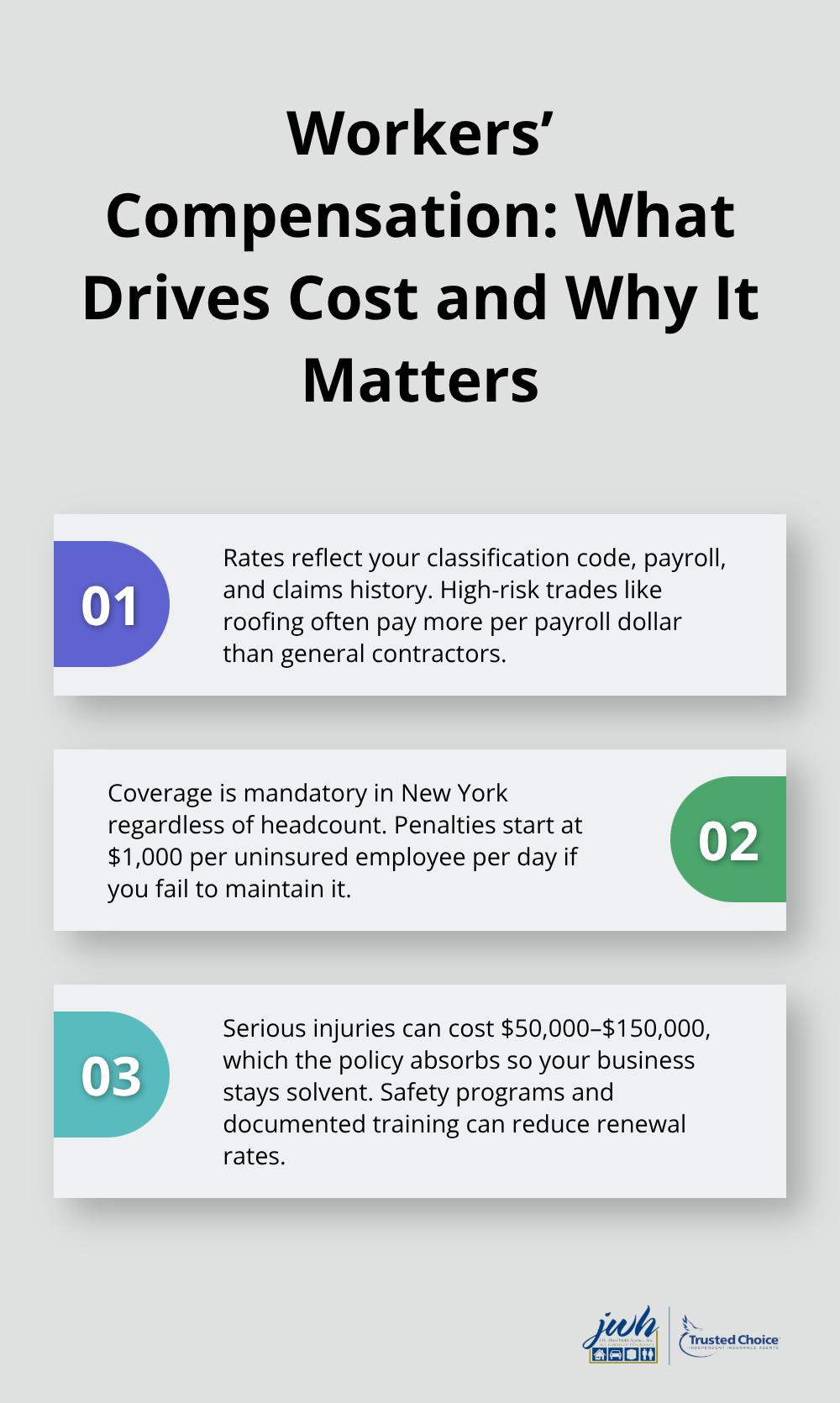

Workers’ Compensation Insurance in New York isn’t optional-it’s mandatory for any contractor with employees, and the cost structure directly reflects your industry segment and safety record. The New York Workers’ Compensation Board sets rates based on your classification code, payroll, and claims history, meaning a roofing contractor pays significantly more per dollar of payroll than a general contractor with similar revenue. If you operate in New York, you must carry this coverage regardless of how many people work for you, and failure to maintain it results in fines starting at $1,000 per uninsured employee per day. A single serious injury claim-such as a worker fracturing a leg at a job site-costs $50,000 to $150,000 in medical bills and lost wages, which Workers’ Compensation absorbs so your business doesn’t collapse.

Safety programs reduce your premiums directly; contractors who invest in OSHA training, site-specific safety protocols, and documented return-to-work programs see measurable rate reductions when their policies renew.

General Liability: Protecting Against Third-Party Claims

General Liability Insurance protects against third-party claims when someone other than your employee is injured or when your work damages client property, covering legal defense costs and settlement amounts up to your policy limit. The state doesn’t mandate a specific minimum limit, but most lenders and property owners require $1 million per occurrence and $2 million aggregate, and projects in Manhattan often demand higher limits like $5 million. This coverage excludes your own equipment and property-Builder’s Risk handles that-so many contractors mistakenly assume General Liability covers everything and then face denial when their own materials burn on site.

Builder’s Risk and Equipment Coverage: Protecting Your Assets

Commercial Property and Equipment Coverage protects the tools, vehicles, and temporary structures you own at job sites, and this is where most contractors discover gaps in their protection. Builder’s Risk policies cover the building under construction and temporary structures like scaffolding against fire, theft, vandalism, and weather damage, but they exclude your hand tools, power equipment, and company vehicles unless you add specific endorsements. A contractor storing $80,000 worth of equipment in a site trailer faces total loss if theft occurs, and standard Builder’s Risk won’t cover it-you need Equipment Coverage or Inland Marine Insurance for that protection. Equipment policies typically cover tools during transport between sites and while stored at job locations, with deductibles ranging from $500 to $2,500 depending on your risk profile and claims history. The construction market is currently in a hard cycle where trade contractors face tightened underwriting and higher premiums, so submitting clean applications with detailed equipment inventories and documented security measures helps you secure better rates.

Commercial Auto Insurance: Coverage for Your Vehicles

Commercial Auto Insurance is separate from your General Liability and covers your company vehicles against accidents, theft, and weather damage, which matters significantly when you transport crews and equipment across New York’s roads-uninsured motorist coverage is especially critical in urban areas where hit-and-run incidents happen regularly. An independent agent representing multiple carriers can identify which endorsements you actually need versus which ones are sales padding, and they’ll coordinate your policies so you don’t pay twice for the same protection or leave dangerous gaps between coverage types. This coordination becomes even more important as your projects grow in complexity and your equipment inventory expands.

Choosing Coverage That Matches Your Actual Projects

Assess Your Project Portfolio and Risk Profile

List every project type you handle over a 12-month period, then rank them by complexity and dollar value. A contractor doing kitchen renovations faces different liability exposure than one managing high-rise facade work, and your insurance needs must reflect that reality. Assess whether you work at heights, handle hazardous materials, operate near occupied buildings, or manage projects over $5 million in value-each factor shifts your coverage requirements upward.

Document your crew size, average payroll, equipment inventory, and subcontractor practices because carriers now differentiate heavily by these specifics rather than treating all contractors as one risk category. The construction insurance market is currently split: general contractors are seeing renewed carrier appetite and stable rates for clean loss histories, while trade contractors face tightened underwriting and higher premiums. This means your application quality determines your outcome.

Submit Complete Applications With Strong Documentation

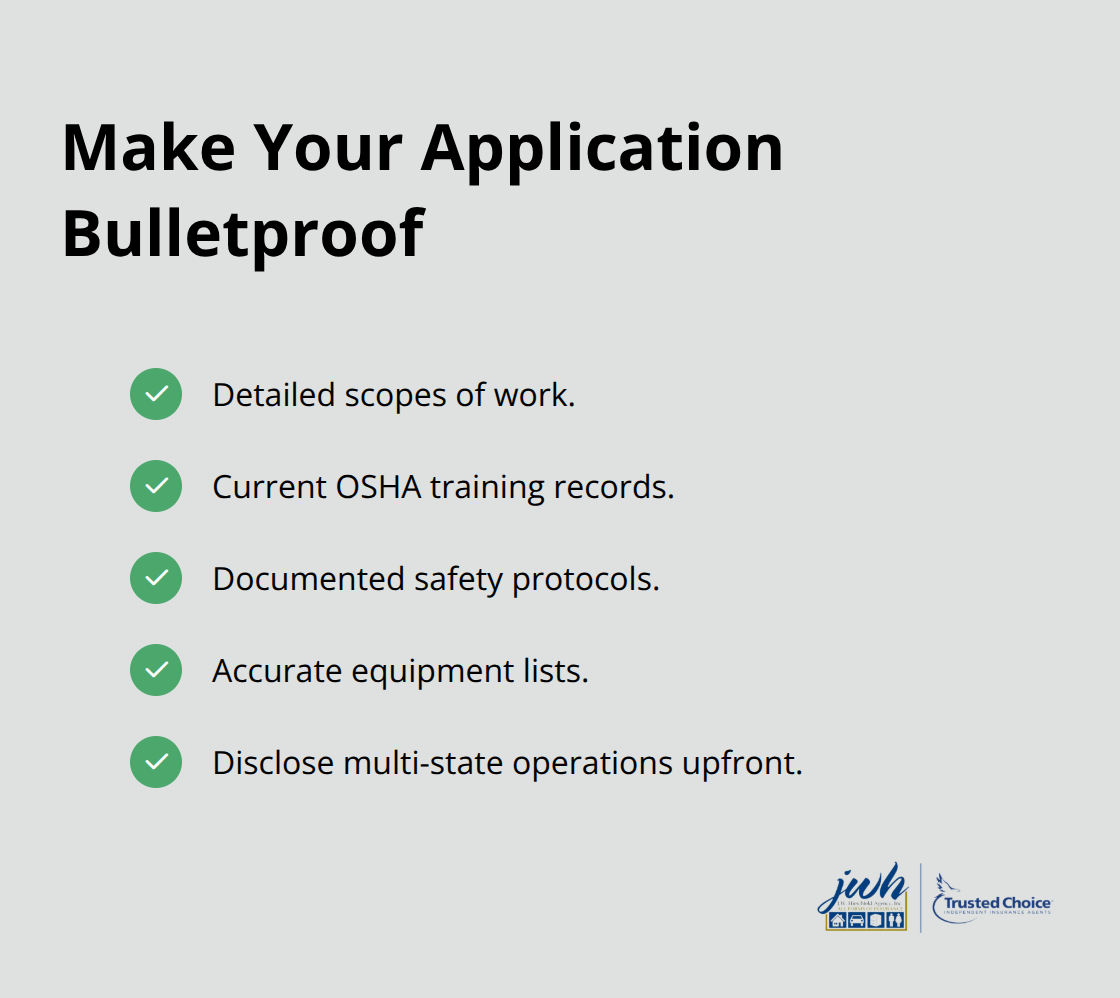

Submit detailed scopes of work, current OSHA training records, documented safety protocols, and accurate equipment lists-incomplete applications get rejected or quoted at penalty rates. If you operate across multiple states, mention that upfront because some carriers offer multi-state programs with better pricing than state-by-state policies. Carriers evaluate your risk based on what you provide, so thorough documentation directly influences whether you receive competitive quotes or face exclusions and rate penalties.

Request Identical Quotes for True Comparison

Comparing quotes requires more than price shopping. Request proposals from at least three carriers, but have them quote identical coverage limits, deductibles, and endorsements so you’re actually comparing apples to apples. Ask each carrier about their claims handling reputation in New York construction-response time and settlement fairness matter far more than saving $500 per year if a claim drags on for months.

Identify Hidden Gaps in Coverage

Pay specific attention to exclusions because that’s where gaps hide. A Builder’s Risk policy might exclude water damage, leaving you exposed if a project site floods during heavy rain. Ask your broker whether soft costs coverage is included, because if your project stalls due to insured damage, you still owe site overhead, equipment rental, and temporary facility costs that can exceed $10,000 per week on larger jobs.

Review whether your General Liability covers contractual liability-many standard policies don’t, but client contracts often require you to assume liability for their negligence, creating exposure your policy won’t cover without an endorsement. An independent agent representing multiple carriers identifies these gaps before you sign, adjusting your coverage limits and deductibles and finding better rates across the board because they’re not locked into one insurer’s limitations. We at JW Hirschfeld Agency, Inc. work with multiple top carriers to uncover exactly these kinds of hidden exposures and tailor your protection accordingly.

Final Thoughts

Contractor insurance in New York shifts as your projects grow, your crew expands, and market conditions tighten around specific trade segments. Workers’ Compensation protects your employees, General Liability shields you from third-party claims, Builder’s Risk covers your project assets, and Commercial Auto handles vehicle losses-but your contractor insurance policy only works when it matches your actual operations, not when you settle for standard templates that leave gaps. The construction insurance market is splitting right now, with general contractors seeing renewed carrier appetite while trade contractors face tighter underwriting and higher premiums, which means your application quality and safety documentation directly determine whether you receive competitive quotes or face exclusions.

An independent insurance agent makes the difference because they represent multiple top carriers and aren’t locked into one company’s restrictions. They identify which gaps apply to your specific work, coordinate your policies so you don’t pay twice or leave dangerous overlaps, and handle claims as your advocate rather than the insurer’s gatekeeper. Unlike captive agents, independent brokers assess your operations across different insurers and find the combination that actually protects your business while keeping your costs competitive.

We at JW Hirschfeld Agency, Inc. work with multiple top carriers to tailor your coverage to your exact needs. Contact us to review your current protection, identify gaps, and secure the contractor insurance policy your business deserves.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.