One accident on a job site can cost you thousands in medical bills, property damage, and legal fees. Contractor liability insurance protects your business from these financial disasters.

At JW Hirschfeld Agency, Inc., we’ve seen how quickly a single incident can threaten a contractor’s entire operation. That’s why understanding your coverage options matters.

What Contractor Liability Insurance Actually Covers

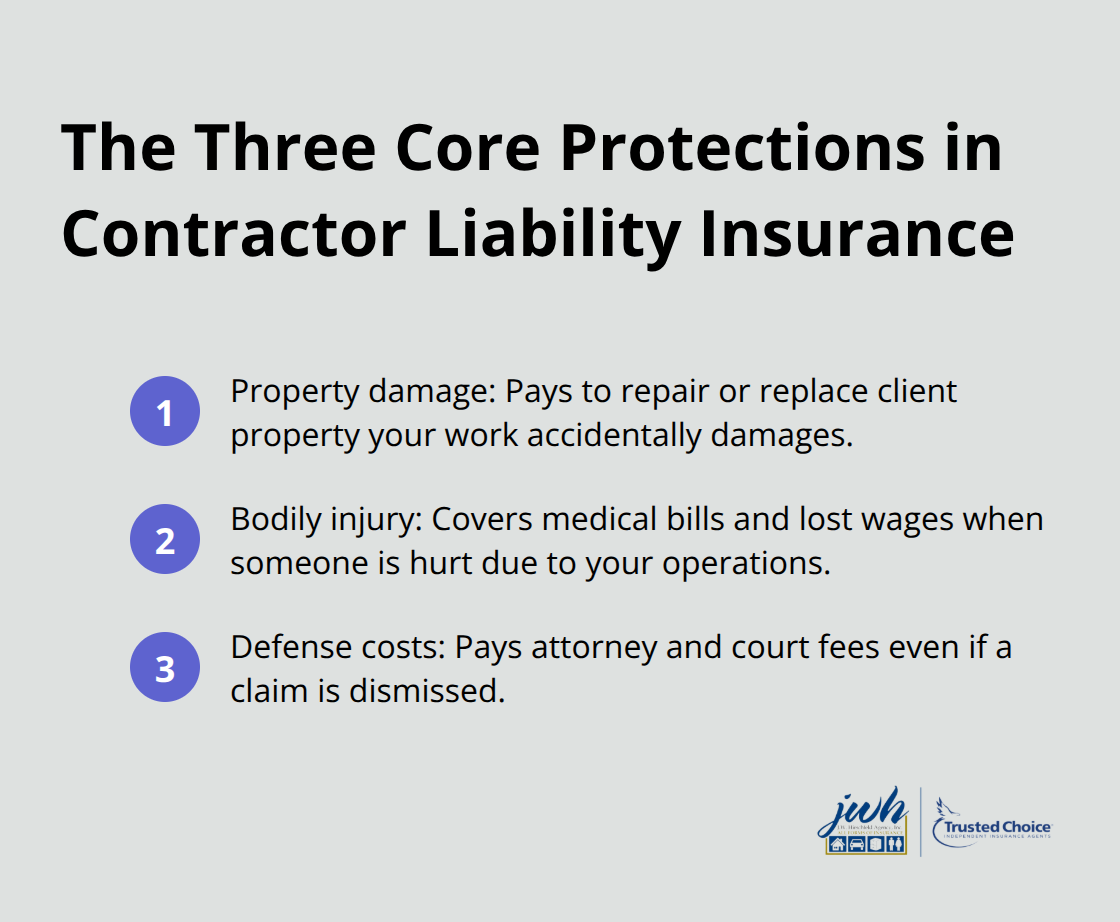

The Three Core Protections Your Business Needs

Contractor liability insurance protects your business against three major financial exposures that show up repeatedly in job site incidents. Property damage claims cover the costs when your work accidentally damages a client’s building, fixtures, or belongings-a ladder punctures a roof, a dropped tool breaks a window, or paint spills on expensive flooring.

Bodily injury liability pays medical bills and lost wages when someone gets hurt because of your work, whether that’s a client’s employee tripping over your equipment, a homeowner slipping on wet surfaces you created, or a third party injured by your negligence on the job site.

Why Defense Costs Matter More Than You Think

Defense costs and legal fees are covered separately, meaning the insurance company pays for your attorney and court expenses even if the claim goes nowhere. This protection alone can save you thousands in legal bills on a contested injury case. Without this coverage, you absorb those costs out of pocket while your business sits idle waiting for resolution.

Meeting Client Requirements and Industry Standards

General liability forms the foundation of contractor protection, and most clients require it before you step foot on their property. Many commercial contracts explicitly demand minimum coverage limits of $1 million per occurrence and $2 million aggregate, with some larger projects pushing those numbers higher. When you work with an independent agent at JW Hirschfeld Agency, Inc., they review your specific job types and recommend tailored limits and endorsements that match your actual exposure rather than selling you a generic one-size-fits-all policy.

Customizing Coverage for Your Specific Work

If you do specialized work-roofing, electrical, demolition-your agent adds coverage for those particular risks. They also handle endorsements like additional insured status for your clients, waiver of subrogation to protect your relationships, and products/completed operations coverage if claims arise months after you finish the job. This layered approach means you avoid overpaying for coverage you don’t need while staying protected against the exposures that actually threaten your business. Understanding what your policy covers is only half the battle; knowing what risks you face on the job site determines whether your coverage truly shields you from financial disaster.

Why Your Business Can’t Operate Without Liability Protection

Construction Sites Create Constant Financial Risk

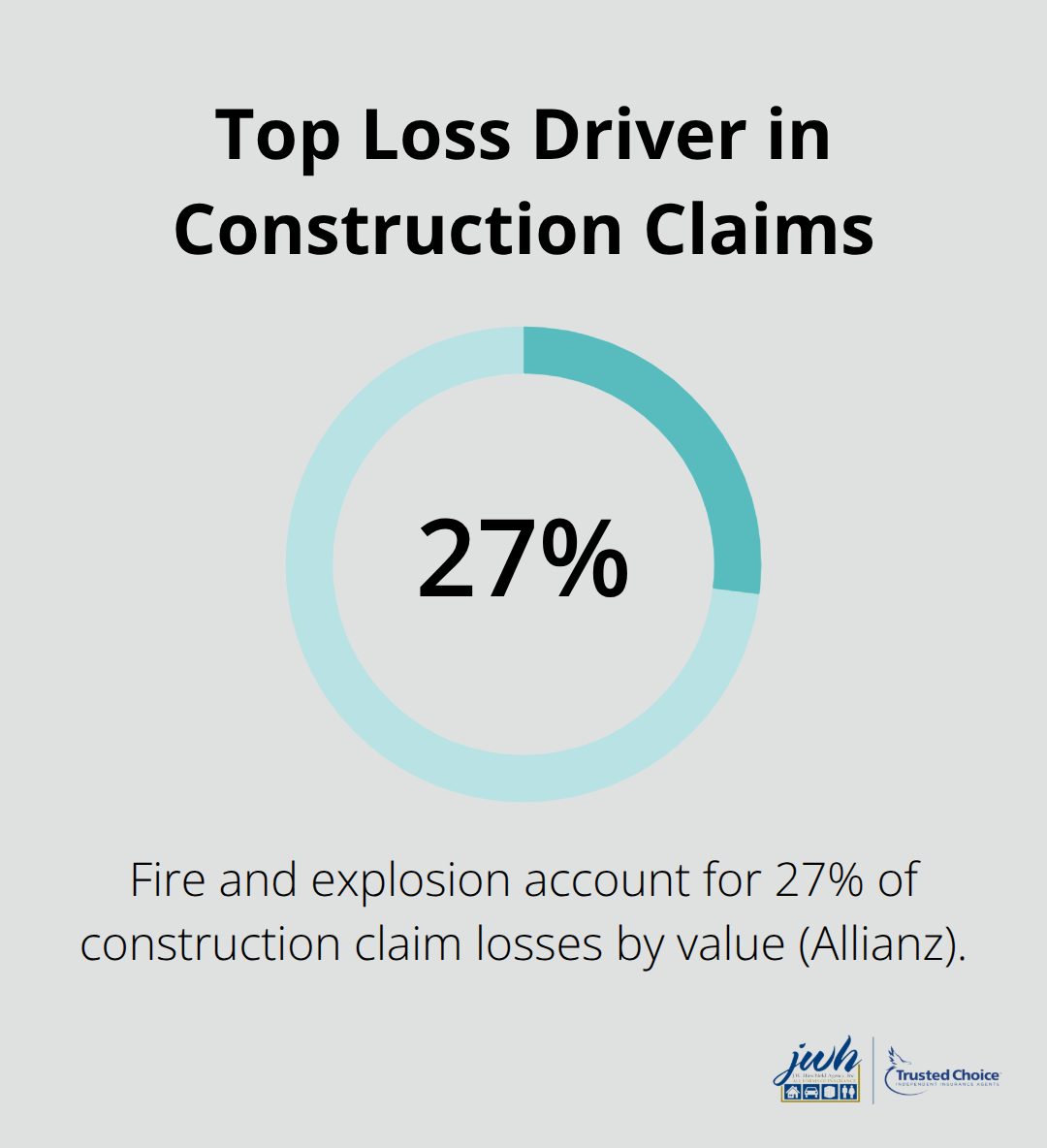

Construction sites generate risk at every moment. A worker trips over your extension cord and breaks an ankle. Your crew accidentally punctures a water line during excavation. A subcontractor’s equipment damages the client’s newly installed flooring. These aren’t hypothetical scenarios-they happen constantly across the construction industry, and each one carries the potential to drain your cash reserves and derail your operation. Fire and explosion claims remain the biggest cause of loss due to the high values associated with engineering and construction projects today. This means major losses hit regularly, not occasionally.

One Claim Can Wipe Out Your Profit Margin

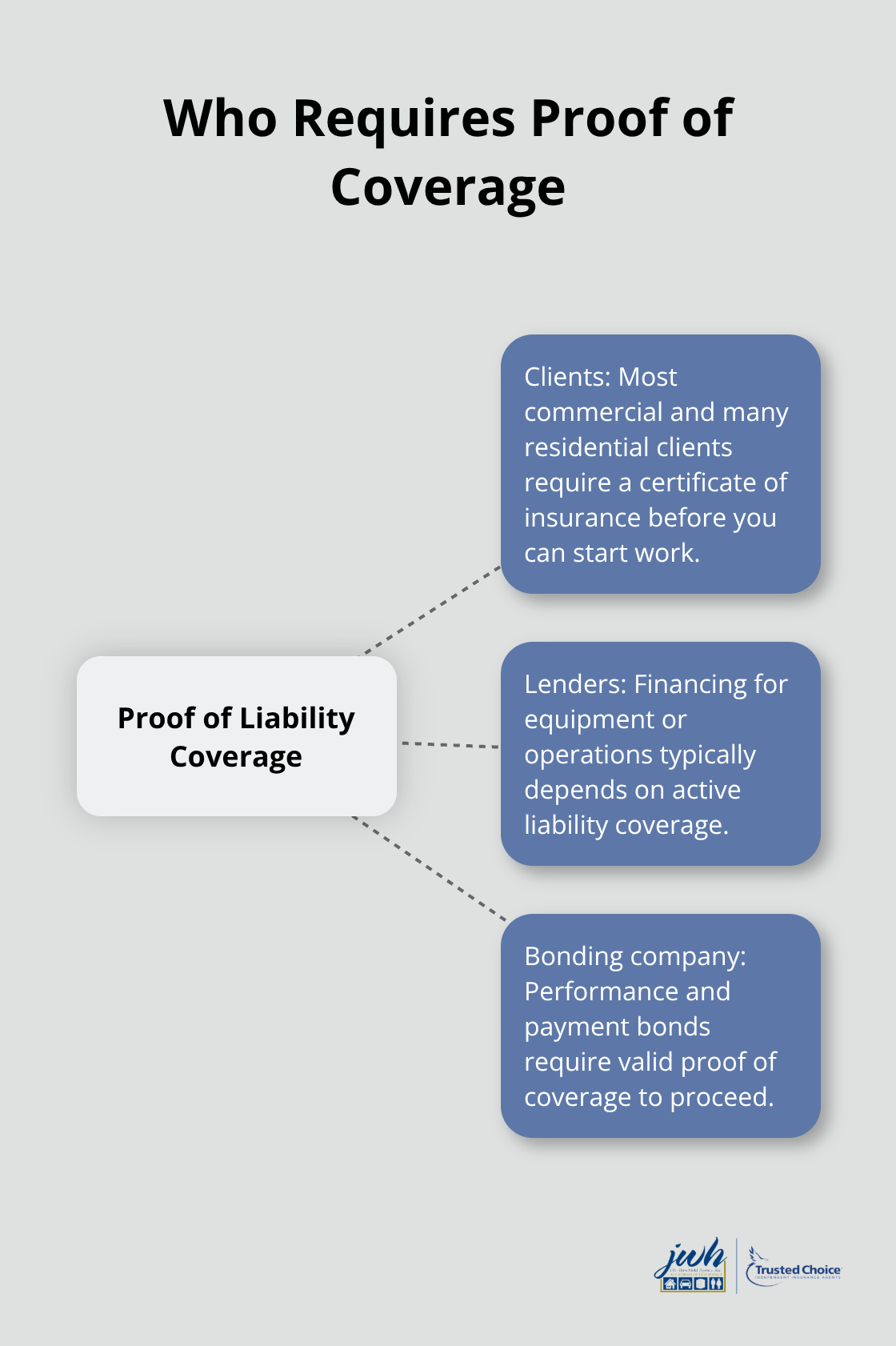

Without liability insurance, a single incident forces you to pay medical bills, repair costs, and legal defense from your operating account. Many contractors operate with thin margins, and one substantial claim wipes out months of profit or forces you to borrow money just to keep working. Your lenders and bonding companies won’t back you without proof of coverage. Most commercial clients won’t let you on their property without a certificate of insurance showing minimum limits of $1 million per occurrence. Residential clients increasingly demand the same protection. If you can’t produce that certificate within 24 hours, you lose the job to a competitor who can.

Clients and Contracts Demand Coverage Before Work Starts

The gap between having coverage and not having it isn’t a matter of saving a few hundred dollars annually-it’s the difference between staying in business and closing your doors after one bad day. Your clients won’t sign contracts without proof of liability protection. Your lenders won’t finance your equipment or operations. Your bonding company won’t back your performance on major projects. These aren’t optional requirements; they’re the price of admission to the construction industry.

Independent Agents Tailor Coverage to Your Actual Exposures

An independent agent understands that a roofing contractor faces different exposures than a demolition specialist, and they tailor your coverage limits, deductibles, and endorsements to match your actual work rather than applying a generic template. They also manage the endorsements clients demand, like additional insured status and waiver of subrogation, so you meet contract requirements without overpaying. When a claim arises, your agent advocates for you through the settlement process to reach a fair outcome, rather than leaving you to negotiate alone with an adjuster. This hands-on approach costs less than you’d spend recovering from a single uninsured or underinsured incident.

Gaps in Coverage Cost More Than You Expect

Many contractors discover too late that their coverage has gaps-missing endorsements, limits that don’t match their contracts, or exclusions that apply to their specific work type. An independent agent prevents those gaps before they become expensive problems. They review your job types, your client contracts, and your actual exposures to build a policy that protects what matters most. This tailored approach means you avoid overpaying for coverage you don’t need while staying protected against the exposures that actually threaten your business. The right coverage structure determines whether your policy truly shields you from financial disaster when an accident happens on the job site.

Common Claims Contractors Face

Injuries on Job Sites Hit Your Bottom Line Hard

Injuries to workers and third parties represent the most frequent claims contractors face. A 2021 study by OnePoll and The Hanover found that 56% of consumers value access to an insurance expert when making coverage decisions, and contractors need that same guidance because site injuries happen constantly. OSHA data shows that construction has one of the highest injury rates across all industries, with falls, struck-by incidents, and caught-between exposures driving thousands of claims annually. Your liability coverage pays medical bills, lost wages, and legal defense when someone gets hurt because of your work-whether that’s a client’s employee tripping over your equipment, a homeowner slipping on wet surfaces you created, or a third party injured through your negligence.

The problem most contractors face is underestimating their exposure limits. A serious injury claim routinely exceeds $500,000 when you factor in ongoing medical care, lost earning capacity, and pain-and-suffering awards. If your policy carries only $300,000 per occurrence, you become personally liable for the difference, and that gap destroys cash flow faster than almost any other business event.

Property Damage Claims Arrive When You Least Expect Them

Property damage claims arrive just as frequently but often catch contractors off guard because they assume their work won’t cause damage. A ladder punctures a roof during installation. Your crew accidentally punctures a water line during excavation. A subcontractor’s equipment damages newly installed flooring. Fire and explosion remain the biggest loss drivers in engineering and construction claims, accounting for about 27% of losses by value according to Allianz Global Corporate & Specialty, which underscores why robust fire protection and hot-work safety protocols matter on every site.

Completed Operations Claims Extend Your Exposure Years Later

Completed operations claims extend your exposure months or even years after you finish a job. A client discovers structural defects, water intrusion, or electrical problems weeks later and files a claim against you. Your policy needs to cover these post-completion incidents because they happen frequently in construction. An independent agent ensures your completed operations endorsement has adequate limits and doesn’t exclude the specific work you perform, which prevents the costly gap where you finish a job, the policy expires, and then a claim arrives with no coverage underneath.

Final Thoughts

Contractor liability insurance protects your business from financial disaster, but only if you have the right coverage in place. Your clients won’t hire you without proof of coverage, your lenders won’t finance your equipment, and your bonding company won’t back your performance on major projects. These aren’t preferences-they’re requirements that determine whether you stay in business or close your doors after a single claim.

The challenge most contractors face is finding coverage that actually matches their specific work rather than paying for a generic policy that leaves gaps. A roofing contractor faces different exposures than a demolition specialist, and your coverage limits, deductibles, and endorsements need to reflect that reality. At JW Hirschfeld Agency, Inc., we represent multiple top carriers, which means we shop your coverage across different insurers to find competitive rates and tailored protection that fits your actual exposures.

When a claim arrives, you don’t face the insurance company alone-we advocate for you through the settlement process to reach a fair outcome. Contact JW Hirschfeld Agency, Inc. to discuss your specific exposures and find the contractor liability insurance protection your business needs to grow without fear.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.