A workplace injury can derail your business operations and drain your finances fast. Workers compensation coverage LI protects your employees when accidents happen while safeguarding your company from devastating liability costs.

At JW Hirschfeld Agency, Inc., we’ve seen too many Long Island business owners operate with gaps in their coverage. The right policy makes all the difference between staying afloat and facing serious financial trouble.

What You Actually Get With Workers Compensation Coverage

Medical Benefits Cover All Treatment Costs

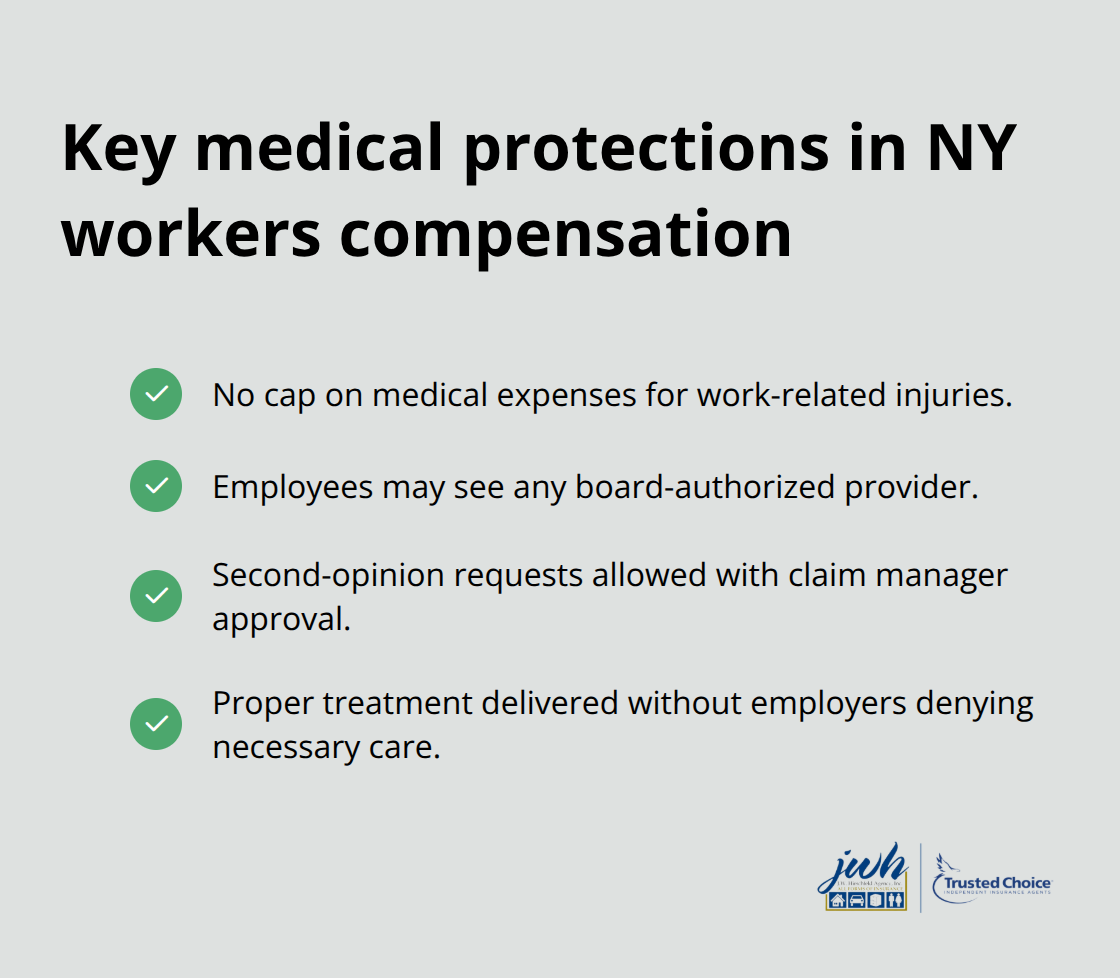

Workers compensation in New York covers three critical areas that protect both your employees and your bottom line. Medical benefits pay for all treatment related to workplace injuries-from emergency room visits to surgery, physical therapy, and ongoing care. New York State requires employers to carry this coverage, and there’s no cap on medical expenses for work-related injuries. Your employees can see any board-authorized provider, and they can request a second opinion with approval from their claim manager. This means your team receives proper treatment without fighting bureaucracy, and you avoid the liability of denying necessary care.

Wage Replacement and Disability Benefits Keep Recovery on Track

Wage replacement benefits activate when injured workers cannot perform their jobs. New York does not replace 100% of wages, so your employees will feel some financial pressure during recovery-this actually incentivizes faster healing and return-to-work. If an injury causes permanent disability, workers receive ongoing benefits based on the severity of their impairment.

Rehabilitation services help workers transition back to work safely through light-duty assignments or modified roles tailored to their physical restrictions. The Stay at Work program reimburses employers for wages and training costs tied to temporary, modified work, which means you maintain productivity while your team recovers. This program works because it aligns everyone’s interests-employees earn wages while healing, you keep operations running, and claims costs stay lower.

Modified-Duty Programs Reduce Claim Costs

Employers who use modified-duty programs effectively report faster return-to-work timelines and reduced overall claim expenses. The key involves documenting restrictions clearly on the Activity Prescription Form so everyone understands what work is safe. Claims notices download on demand through the New York Workers Compensation Board system, giving you real-time visibility into claim status and decisions.

An independent agent helps you structure policies that maximize these return-to-work opportunities and identifies which job classifications qualify for modified-duty roles. This transforms what seems like a burden into a practical recovery tool. The next section explores why this coverage matters so much for Long Island businesses-and what happens when you don’t have the right protection in place.

Why Your Business Needs Workers Compensation Coverage Now

New York State Mandates Coverage-Violations Cost Heavily

New York State law requires employers to carry workers compensation coverage, and the New York Workers Compensation Board enforces this requirement strictly. Employers operating without coverage face civil penalties that escalate quickly, plus potential criminal charges if an injury occurs. The financial exposure extends far beyond fines-uninsured employers become personally liable for all medical costs and lost wages when an employee is injured, which can easily exceed $100,000 for a serious workplace accident. Long Island businesses operating without proper coverage essentially bet their company on never experiencing a workplace injury, which is not a sustainable business strategy.

Serious Injuries Create Catastrophic Financial Exposure

Workers compensation coverage protects your cash flow and operational stability when injuries happen. A single serious workplace injury without coverage can force a business to close permanently. Medical expenses for workplace injuries typically range from $10,000 to $50,000 for moderate injuries and can exceed $500,000 for catastrophic cases like spinal cord damage or amputation. Wage replacement obligations add substantial ongoing costs when workers cannot perform their jobs.

Without coverage in place, these costs fall directly on your business and drain resources that should support growth and operations.

Employee Retention Depends on Safety Investment

Your employees notice whether you carry proper coverage-workers compensation demonstrates that you invest in their safety and wellbeing, which directly impacts retention and morale. Businesses with strong workers compensation programs report lower voluntary turnover rates because employees feel protected and valued. Workers want to know their employer will support them if an accident happens, and coverage sends that message clearly. This protection becomes especially important for Long Island businesses competing for skilled workers in tight labor markets.

Independent Agents Match Coverage to Your Actual Risks

An independent agent helps you navigate New York’s specific coverage requirements and identifies gaps that could expose your business to liability. Independent brokers represent multiple carriers, meaning they find the most affordable premium for your industry classification and workforce structure rather than steering you toward one company’s products. This personalized approach ensures your coverage matches your actual operational risks, whether you employ seasonal workers, remote staff, or field teams working across different job sites. The next section examines common coverage gaps that leave many Long Island businesses exposed despite thinking they have adequate protection.

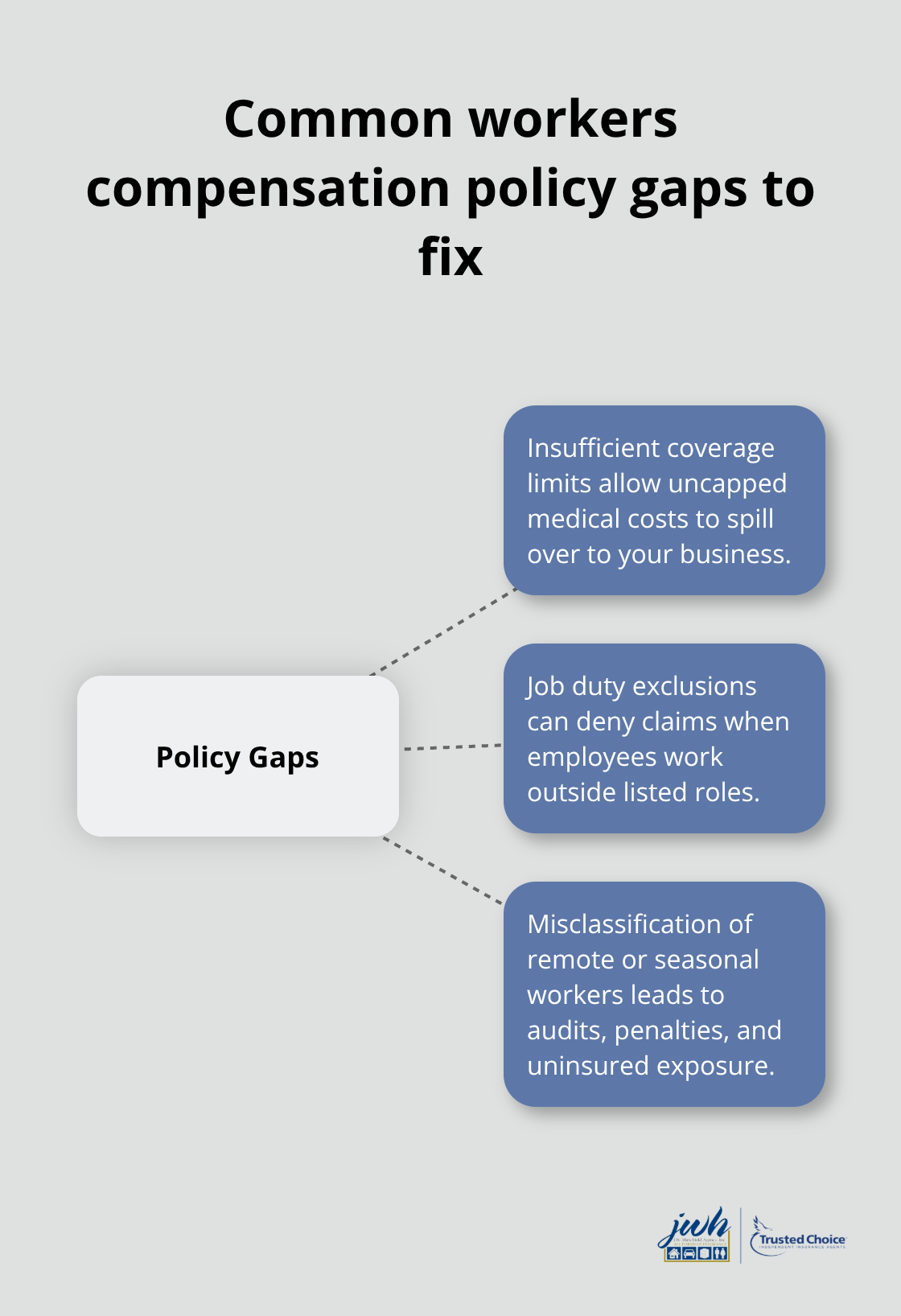

Common Gaps in Workers Compensation Policies

Most Long Island business owners believe their workers compensation policy protects them completely, but standard policies contain significant gaps that expose companies to unexpected liability. Many employers discover these gaps only after an injury occurs and a claim gets denied. The New York Workers Compensation Board processes thousands of claims annually, and disputes over coverage limits and job duty exclusions represent a consistent source of employer financial exposure.

Insufficient Coverage Limits Create Hidden Liability

Insufficient coverage limits rank as the most dangerous gap because New York allows medical expenses for workplace injuries to accumulate without caps. A construction accident resulting in spinal fusion surgery, physical therapy, and ongoing pain management can easily exceed $300,000 in medical costs alone. If your policy caps medical benefits at $100,000 or $150,000, your company becomes liable for the overage.

This exposure catches many business owners off guard because they assume their carrier covers all work-related medical expenses. The reality is that you must actively negotiate appropriate limits based on your industry classification and workforce composition. Carriers often propose conservative limits to reduce their risk, which shifts that risk directly to your business.

Job Duty Exclusions Leave Gaps During Staffing Changes

Job duty exclusions create another critical problem because policies often exclude coverage for work performed outside normal job classifications. An employee who temporarily performs duties outside their standard role during staffing shortages may fall outside coverage if an injury occurs during that work. This happens frequently in small businesses where team members cross job functions regularly.

Your policy language determines whether coverage applies when employees work outside their primary roles. Many standard policies contain restrictive language that excludes coverage for duties not explicitly listed in the job classification. During busy seasons or unexpected absences, your team naturally shifts responsibilities-but your coverage may not shift with them.

Misclassification of Remote and Seasonal Workers

Remote and seasonal workers present the third major gap because many employers fail to report these workers to their carriers or classify them incorrectly. The New York Workers Compensation Board requires employers to report all workers, including part-time, temporary, and remote staff. Misclassification results in premium audits that reveal unpaid premiums plus penalties, and it leaves your company uninsured for those workers if an injury occurs.

An independent agent reviews your actual workforce structure and operational practices to identify these gaps before they become expensive problems. Independent brokers representing multiple carriers can customize your coverage limits and exclusions based on your specific operations rather than accepting standard policy language. This personalized approach costs far less than discovering gaps during a claim dispute or facing penalties from the New York Workers Compensation Board for misclassified workers.

Final Thoughts

Workers compensation coverage LI protects your business from financial devastation while showing your team that you prioritize their safety. The gaps we outlined-insufficient limits, job duty exclusions, and misclassified workers-represent real risks that expose Long Island businesses to unexpected liability and regulatory penalties. Standard policies rarely address your specific operational challenges, which means accepting boilerplate coverage almost guarantees exposure.

This is where independent agents make a measurable difference. We at JW Hirschfeld Agency, Inc. represent multiple top carriers, so we negotiate coverage tailored to your actual business operations rather than steering you toward one company’s limited options. We review your workforce structure, job classifications, and operational practices to identify gaps before they become expensive problems, catching the details that standard policies miss (remote workers, seasonal staff, temporary duty assignments, and industry-specific risks that require customized limits and exclusions).

Contact JW Hirschfeld Agency, Inc. for a comprehensive workers compensation review. We’ll examine your current coverage, identify gaps specific to your operations, and find competitive pricing from multiple carriers. Let us help you build coverage that actually protects your business.

The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.

Artificial intelligence may have been used to generate text and images in some blog articles.